What Are The Most Common Debt Solutions?

Debt relief can alleviate the problems associated with an overwhelming credit card debt or personal loans. While it may not always be right for everyone, it sure can work for others. What are the most common debt solutions? This article discusses some of the ways to help you ease the burden of debt.

Debt relief can alleviate the problems associated with an overwhelming credit card debt or personal loans. While it may not always be right for everyone, it sure can work for others. What are the most common debt solutions? This article discusses some of the ways to help you ease the burden of debt.

Should You Seek Debt Relief?

Have you been struggling with debt along with other financial obligations? If you think there’s no hope to repay your unsecured debt such as credit cards or personal loans albeit you’ve cut spending, then you might want to consider getting debt relief.

Common Debt Solutions to Consider

Should you decide to get debt relief to repay all of your credit card debt, please ensure that you know what you need to qualify, the tax implications and which creditors are being paid. Below are some of the options you might want to consider for debt relief:

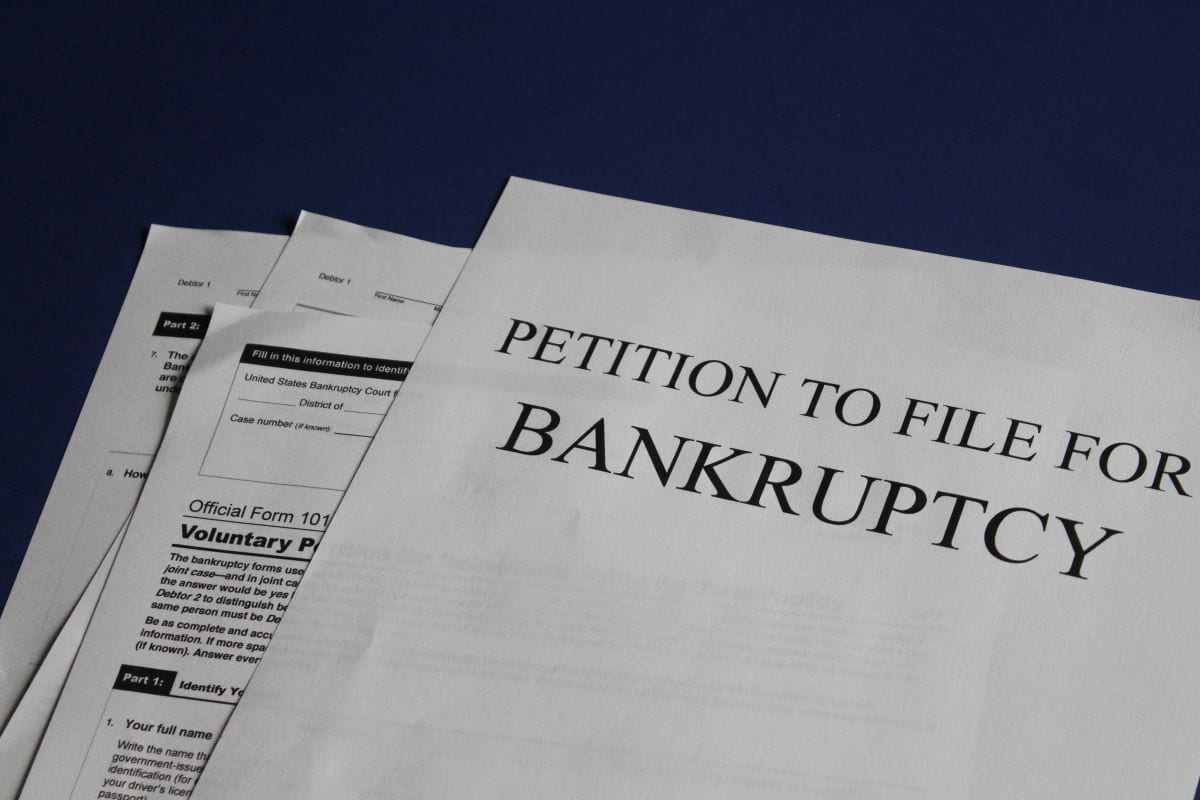

Bankruptcy

Under the protection of a federal court, Chapter 7 Bankruptcy can wipe out several forms of debt including credit card debt, personal loans and medical bills. However, you may have to give up some of your assets like a car or jewelry.

Filing for bankruptcy is one of the most common and also effective (if you qualify) in erasing overwhelming debt. But keep in mind that you’ll need to pass the means test and you haven’t filed a Chapter 7 bankruptcy in the past eight years.

You may be able to complete the process in about six months or less. First, complete a pre-file bankruptcy counseling from a qualified professional within 180 days before application. Look for an attorney for assistance and file all the paperwork. A trustee will need to review all paperwork and confirm if you are eligible for Chapter 7 Bankruptcy. You may have to sell your assets and the proceeds go to the creditor. Properties held as collateral may be returned to your creditors.

Debt Settlement

If you don’t qualify for bankruptcy, you may want to consider a debt settlement to settle unsecured credit card debt or personal loans. Debt settlement is an agreement between you and the lender for a one-time payment in full of a reduced amount to clear your existing debt balance.

This debt relief option can help you repay your debt faster. For some people, it can avoid filing for bankruptcy and surrendering your assets. While it’s not going to miraculously end your financial troubles, it’s a good option. You can learn more about this option from FreedomDebtRelief.com and similar companies.

Debt Management Plans

Having a debt management plan allows you to settle credit card debts in full but with reduced interest rates. You make payments to a financial or credit counseling agency and they can distribute these to the financial companies you owe money to.

With a debt management plan, your credit accounts are closed, which means you’ll have to live without a credit card until you fully pay or complete the plan.

If you’re serious about reducing or eliminating debt, then get in touch with one of our professionals for debt relief.

Are You Ready to Eliminate Credit Card Debt?

Freedom Debt Relief has the solution to your financial problems. We can help you reduce or completely eliminate your debt. However, we suggest that you commit to this option to ensure positive results. What are the most common debt solutions? Talk to us so we can help you make an informed decision on how to go about your overwhelming debt.

I am a

I am a  Mr. David M. Offen, Esq. is a bankruptcy and

Mr. David M. Offen, Esq. is a bankruptcy and  The number of small businesses filing for bankruptcy increases every year, and while bankruptcies don’t always lead to the full closure of the company, in a lot of cases they do. If your dream business is currently on the verge of bankruptcy, don’t panic. There are some steps you can take that may help you to turn things around. Try to think as positively as you can and put the following steps into action.

The number of small businesses filing for bankruptcy increases every year, and while bankruptcies don’t always lead to the full closure of the company, in a lot of cases they do. If your dream business is currently on the verge of bankruptcy, don’t panic. There are some steps you can take that may help you to turn things around. Try to think as positively as you can and put the following steps into action.