Top 5 Best Long-Term 529 Plans 2026: Midwest Rankings & Tax-Smart Picks

When you open a 529, you’re picking a long-term partner for your child’s future. The right plan compounds tax-free, keeps fees low, and delivers deductions that feel like a yearly rebate.

Midwestern savers enjoy the best of both worlds: rich state perks and several nationally elite, low-cost plans. But new rules—from K–12 tuition to Roth rollovers—add complexity.

This guide cuts through the noise. We’ll share our 2026 data-backed scoring rubric, then spotlight five plans that lead on returns, cost, and tax breaks, so you know exactly where your next college-fund dollar belongs.

Let’s get started.

How We Built the 2026 Midwest 529 Scoreboard

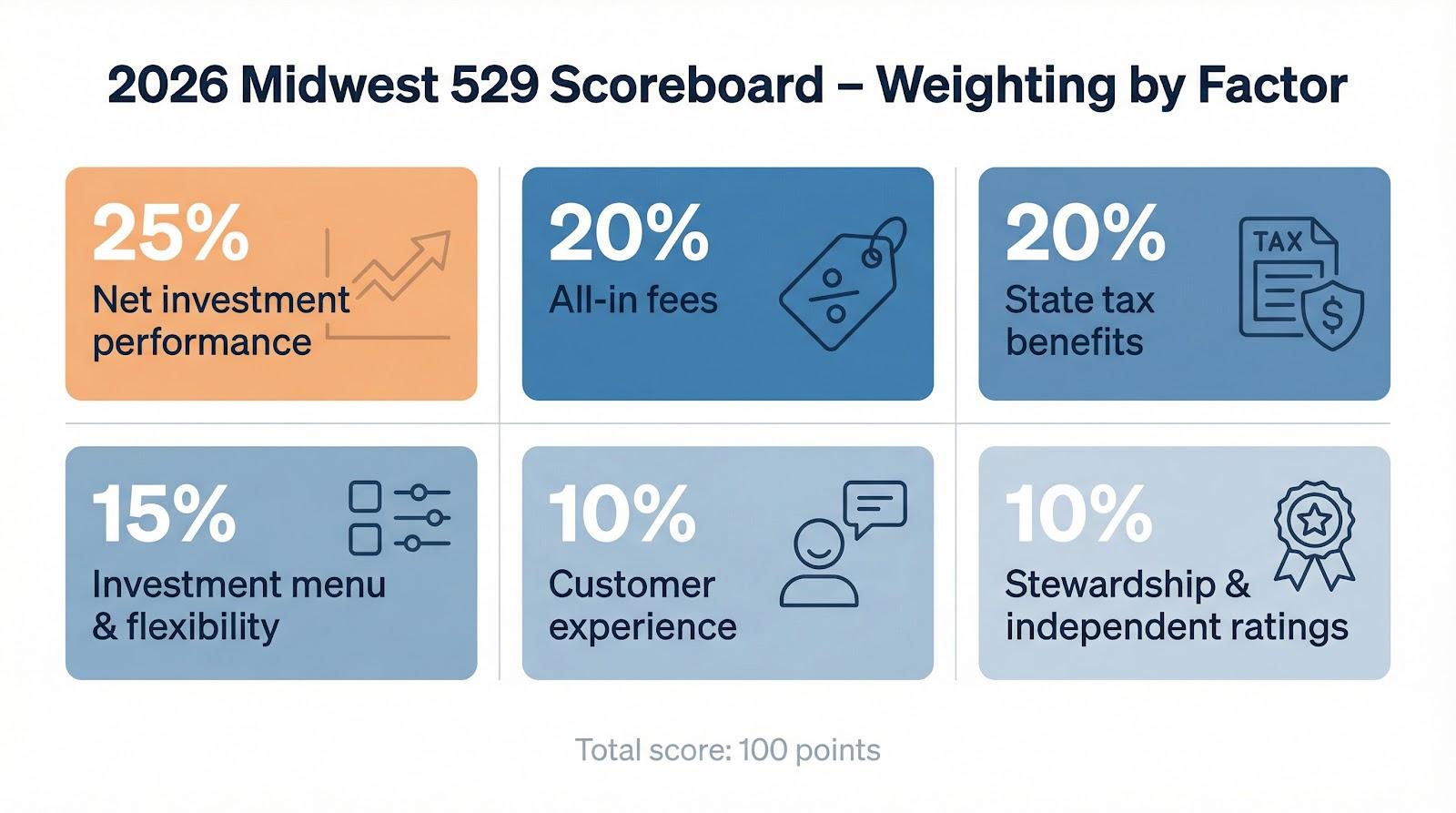

First, we treated each 529 plan like a mutual-fund analyst: every data point fed a rubric, and each score rolled up to a clean 100-point scale. That keeps our praise and our criticism anchored in data, not gut feel.

We pulled fresh figures from Q4 2025 plan disclosures, Morningstar medal reports, and state-treasurer filings. Performance covers one-, three-, and five-year returns for the default age-based portfolios. Fee data include program, underlying-fund, and state-administration charges. Tax rules were double-checked against Savingforcollege’s latest state guide, which also flags the nine tax-parity states—Kansas and Ohio among them—that reward residents for any 529 contribution, not just their home plan.

Here’s the weight grid we used:

- Net investment performance – 25 percent

- All-in fees – 20 percent

- State tax benefits – 20 percent

- Investment menu and flexibility – 15 percent

- Customer experience – 10 percent

- Stewardship and independent ratings – 10 percent

Each factor is normalized, then multiplied by its weight. The math produces a single score that lets a high-performing, no-frills plan compete with a flashier option that leans on bigger tax perks.

Scores reset every year, so a plan that trims expenses or upgrades digital tools can jump ahead quickly. That pressure works in your favor: Midwest plans keep refining, and savers reap the reward.

1. Illinois Bright Start 529 College Savings Plan

Illinois families have already set aside more than $12.5 billion through the Illinois Bright Start 529 College Savings Plan, proof that Bright Start checks every box. Morningstar has stamped it Gold again, and the state treasurer keeps pushing manager TIAA to shave costs and polish the tech. In late 2024 expenses fell about thirteen percent and a clean mobile app arrived, so you can nudge contributions or share a gifting link while waiting in the school pick-up line. Illinois families also pocket one of the richest deductions in the nation: up to ten thousand dollars for single filers or twenty thousand dollars for joint filers each year. That money stays in your pocket today and still grows tax-free tomorrow.

Performance holds up its end of the deal. The age-based “Enrollment Year” tracks have outpaced benchmark blends over one-, three-, and five-year windows, and they do it with index-fund pricing that would make many exchange-traded funds blush. Vanguard, DFA, and other best-of-breed managers sit side by side, giving the portfolio depth instead of a single-brand lineup.

| Metric | Bright Start Direct |

|---|---|

| Five-year annualized return | about six point eight percent (age-based average, net) |

| All-in expense ratio | zero point one zero percent after the 2024 cut |

| State tax break | deduct ten thousand dollars single or twenty thousand dollars joint |

| Minimum to open | none |

| Account cap | five hundred fifty thousand dollars per beneficiary |

| Morningstar rating | Gold (seventh year) |

- Cost leadership. Only Utah’s my529 comes close on price, but Bright Start wins the tiebreaker with its rich in-state tax perk.

- Investor-friendly oversight. The treasurer’s office has pushed three fee cuts in seven years and added a newborn seed grant—clear signs that savers come first.

- Flexibility without friction. No enrollment fee, no minimum, and a slick app make consistent saving almost effortless.

K–12 tuition withdrawals are still taxed by Illinois, so if private-school funding is on your horizon you may want a secondary out-of-state 529 for that slice. For traditional college timelines, though, Bright Start is tough to top.

2. Ohio CollegeAdvantage 529 Savings Plan

CollegeAdvantage is a workhorse that delivers where it counts: net returns and low costs. The program fee sits at zero point one three percent, with a token zero point zero two percent state charge layered on top. That puts the all-in expense near zero point one five percent, cheaper than many index mutual funds. Add five-year performance a touch above seven percent and you have a compounding machine that quietly outruns pricier rivals.

Tax treatment is the kicker. Ohio lets residents deduct up to four thousand dollars per child each year and, crucially, applies that break to any 529 plan. The fact that more than half of Buckeye savers still choose CollegeAdvantage shows the in-state option is already best in class.

Investment choice is broad but not overwhelming. Three risk-graded age-based tracks handle autopilot investors, while seventeen static portfolios cover everything from all-equity to an FDIC-insured savings option. Vanguard and Dimensional funds form the backbone, keeping expenses low and index tracking tight.

The website focuses on function over flash. You can schedule automatic drafts, link Upromise rewards, and share a gifting link with grandparents who still write paper checks. Nothing fancy, just smooth enough to keep contributions flowing.

| Metric | CollegeAdvantage Direct |

|---|---|

| Five-year annualized return | about seven point one percent (age-based average) |

| All-in expense ratio | zero point one five percent |

| State tax break | four thousand dollars per beneficiary; unlimited carry-forward |

| Tax parity | yes, deduction applies to any plan |

| Morningstar medal | Silver |

Two quick tips before we move on. First, front-loading a newborn’s account can create years of deductions thanks to Ohio’s carry-forward rule. Second, double-check that you are in the direct plan; the advisor-sold version carries a very different fee schedule.

3. Michigan Education Savings Program (MESP)

MESP often goes unnoticed, yet the numbers land it on any short list. Costs sit near zero point one seven percent—slightly above Illinois and Ohio—and the plan’s age-based portfolios have averaged about six point five percent a year over the past five. When every extra tenth of a percent compounds for eighteen years, that balance between fee and return matters.

Michigan sweetens the deal with a state deduction worth up to five thousand dollars for single filers or ten thousand dollars for couples. At the flat four point two five percent state income-tax rate, that is a built-in credit of roughly two hundred twelve to four hundred twenty-five dollars every year you contribute.

Investment choice is straightforward. Three enrollment tracks—Active, Index, and Blend—let you pick a philosophy once and move on. Six static options cover specialists who want all-US equity, extra international exposure, or a conservative bond tilt. All portfolios sit on the same TIAA chassis that powers Bright Start, so the interface and automation tools feel familiar: painless recurring drafts, gifting links, and a college-cost calculator that shows whether you are on pace or need to adjust contributions.

| Metric | Michigan MESP |

|---|---|

| Five-year annualized return | about six point five percent (age-based average) |

| All-in expense ratio | zero point one three to zero point one eight percent (track dependent) |

| State tax break | five thousand dollars single or ten thousand dollars joint |

| Minimum to open | none |

| Maximum balance | five hundred thousand dollars per beneficiary |

| Morningstar medal | Silver |

Two perks deserve a spotlight. First, Michigan offers periodic matching grants or bonus deposits during 529 Day promotions, nudging families to start early. Second, the generous maximum balance makes the plan attractive for aggressive savers.

The trade-off? MESP has no ESG or specialty tracks, and K–12 tuition withdrawals trigger a state-tax clawback. If private school is in your plan, park that money in an out-of-state 529. For four-year college savers, though, MESP provides a simple path to long-term growth.

4. Wisconsin Edvest 529 College Savings Plan

Edvest was once the quiet option among Midwest plans, but two fee cuts and a refreshed glidepath have changed the story. The index track now costs about zero point two zero percent, and five-year returns sit near six point seven percent, good enough for a national top-quartile slot.

Wisconsin rewards savers with an inflation-linked deduction of five thousand two hundred eighty dollars per beneficiary for the 2026 tax year. A family with two children can shelter more than ten thousand five hundred dollars, trimming roughly five hundred twenty-five dollars from their state bill at the five percent rate. Stretch that perk over fifteen years of contributions and you build a tidy stack of tuition money.

Investment choice is broad without feeling like a buffet. Three enrollment tracks—Index, Active, and Principal Protection—cover most risk levels. Seventeen static options add specialty slices such as small-cap value, international equity, and a guaranteed stable-value fund for grandparents who prefer zero volatility.

| Metric | Wisconsin Edvest |

|---|---|

| Five-year annualized return | about six point seven percent (age-based average) |

| All-in expense ratio | about zero point two zero percent on the index track |

| State tax break | five thousand two hundred eighty dollars per beneficiary (2026) |

| Rollover deduction | yes, incoming rollovers count as contributions |

| Morningstar medal | Bronze |

Small touches push Edvest forward. Roll money in from another state’s 529 and that amount counts toward your deduction, effectively paying you to switch. Gifts are simple: relatives click a link, choose credit card or ACH, and the plan often waives processing fees during 529 Day promotions.

Where does Edvest fall short? The active track creeps toward zero point three zero percent, and Morningstar still awards only a Bronze for governance depth. If you want Gold-level stewardship, stick with Illinois or Ohio. For a low-cost plan paired with a flexible state perk, though, Edvest earns its seat at the table.

5. Kansas Learning Quest 529 Education Savings Program

Kansas offers a rare deal: it gives residents a tax break for any 529 plan, then challenges them to find a better option than Learning Quest. Most stay put because the home plan delivers solid value.

Fees on the index track land around zero point two two percent, and five-year returns average about six point four percent. The plan is managed by American Century, headquartered in Kansas City, so oversight meetings happen close to the state treasurer’s office—a subtle but helpful layer of accountability.

The annual deduction is modest—three thousand dollars for single filers or six thousand dollars for joint filers—yet it still trims a few hundred dollars from most state tax bills. More important, Kansas belongs to the small group of tax-parity states, so if another plan truly fits you better, you keep the deduction anyway. That competitive pressure keeps Learning Quest sharp.

Choice is the headline. Three age-based glidepaths come in both index and active flavors, and twenty static portfolios include an ESG equity option for socially conscious savers. There is even a conservative bank-savings portfolio for college-in-two-years money.

| Metric | Learning Quest Direct |

|---|---|

| Five-year annualized return | about six point four percent (age-based average) |

| All-in expense ratio | zero point two zero to zero point two five percent |

| State tax break | three thousand dollars single or six thousand dollars joint on any plan |

| ESG portfolio | yes |

| Morningstar medal | Bronze |

Two tactical notes. First, rollovers from another 529 count as new contributions, unlocking a fresh Kansas deduction. Second, if you reach the deduction limit early in the year, you can send additional dollars to an ultra-low-cost plan like Illinois Bright Start; Kansas will still honor next spring’s break on the first six thousand dollars you invested at home.

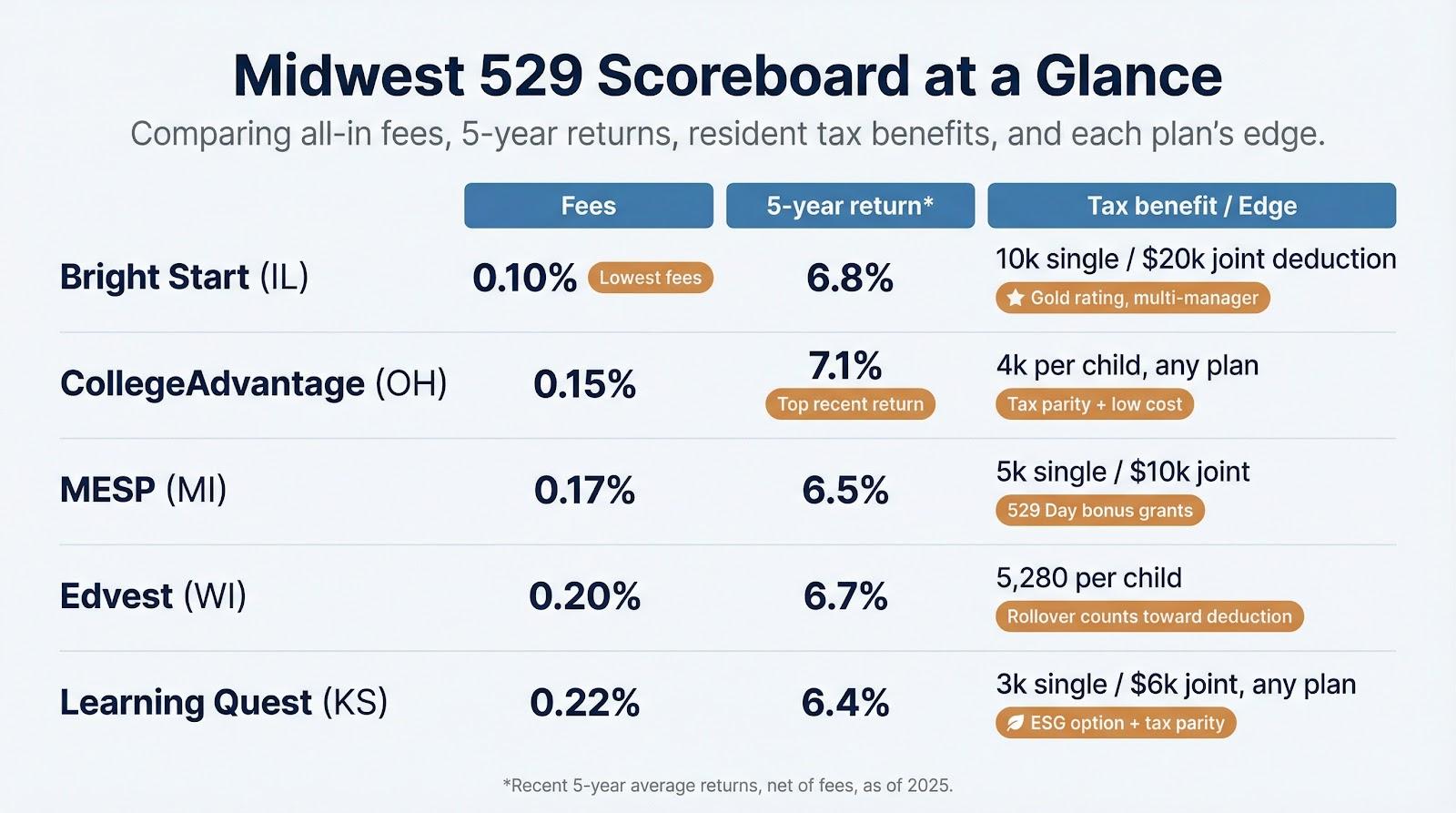

Midwest 529 Scoreboard at a Glance

Five plans, five solid choices, yet each leans on a different blend of cost, return, and tax relief. Scan the table, then match the numbers to your priorities. If you want the absolute floor on fees, Illinois leads. Need tax flexibility because you might relocate? Kansas or Ohio stand out. Looking for a newborn seed grant? Michigan checks that box.

| Plan | All-in fees | Five-year return* | Resident tax benefit | Notable edge |

|---|---|---|---|---|

| Bright Start (IL) | zero point one zero percent | six point eight percent | deduct ten thousand dollars single or twenty thousand dollars joint | Morningstar Gold, multi-manager lineup |

| CollegeAdvantage (OH) | zero point one five percent | seven point one percent | deduct four thousand dollars per child, any plan | Tax parity and low cost |

| MESP (MI) | zero point one seven percent | six point five percent | deduct five thousand dollars single or ten thousand dollars joint | Periodic 529 Day bonus grants |

| Edvest (WI) | zero point two zero percent | six point seven percent | deduct five thousand two hundred eighty dollars per child | Rollover counts toward deduction |

| Learning Quest (KS) | zero point two two percent | six point four percent | deduct three thousand dollars single or six thousand dollars joint, any plan | ESG portfolio and tax parity |

*Returns represent average annual performance of each plan’s principal age-based track, net of fees, from 2021 to 2025.

Only about one percentage point separates these plans on recent returns, and fee spreads are measured in basis points. That puts the spotlight on state perks and secondary features. A high deduction, such as Illinois’s, can outweigh fee gaps for large contributors, while Kansas’s parity rule lets mobile families shop around without penalty.

Choose the column that matters most to you, then continue. The next section answers real-world questions, such as whether to chase an out-of-state plan and how the new rollover rules affect overfunding decisions.

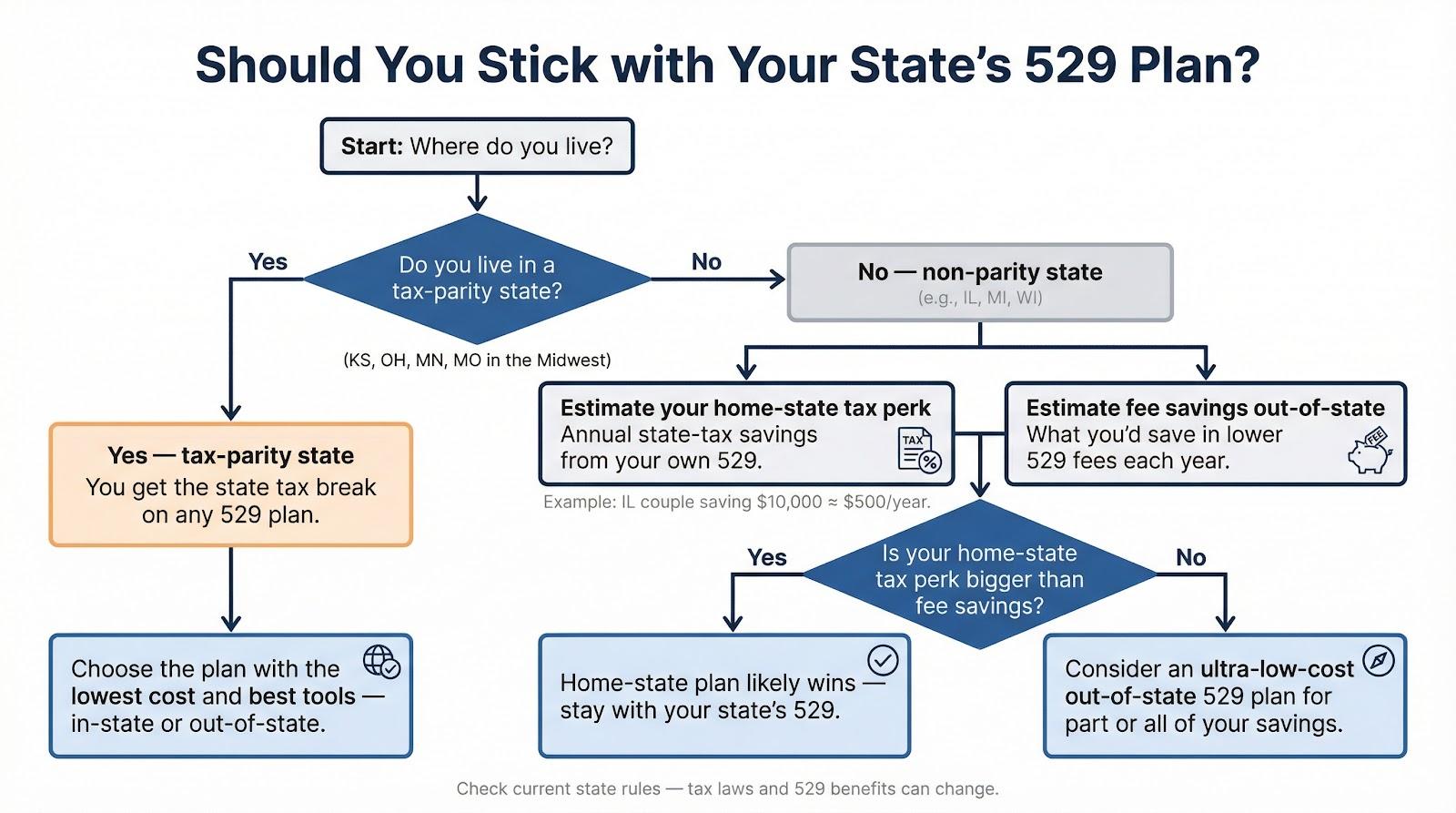

1. Should I stick with my state’s plan or chase lower fees elsewhere?

Run the numbers first. An Illinois couple saving 10,000 dollars a year pockets a 500-dollar state-tax discount every December. Over fifteen years that benefit often outweighs the few basis points you would save by moving to Utah’s plan. The exception is the group of nine tax-parity states—Kansas, Ohio, Minnesota, and Missouri in our region—where you get the deduction no matter which plan you use. If you live in one of those, choose the plan with the lowest cost and best tools.

2. What if we overfund and Junior wins a full ride?

Congress created a clean exit. Under the 2022 SECURE 2.0 Act, you may roll up to 35,000 dollars from a 529 that has been open at least fifteen years into the beneficiary’s Roth IRA, free of tax and penalty, subject to annual Roth limits. Extra savings can become retirement seed money instead of a costly mistake.

3. Can 529 money pay for K–12 tuition?

Federally, yes—up to 20,000 dollars per child each year starting in 2026. States differ. Ohio, Wisconsin, and Kansas follow the federal rule with no clawback. Illinois and Michigan still treat K–12 withdrawals as non-qualified for state tax, so you would repay prior deductions on that slice. If private school is in the plan, open a secondary 529 in a parity state to keep flexibility without risking your home-state break.

4. Will a big 529 crush our financial-aid chances?

Hardly. Parent-owned 529s count as a parental asset on the FAFSA and are assessed at a maximum of five point six four percent. Put another way, every 10,000 dollars in a 529 reduces aid by at most 564 dollars. Student-owned assets are hit at 20 percent, so keeping the account in the parents’ name is already kinder. Beginning with the 2024–25 FAFSA, distributions from grandparent-owned 529s no longer appear as student income, closing the old “grandparent trap.”

5. When should we stop contributing?

Aim to have roughly 75 percent of your goal funded by junior year of high school. At that point market swings matter more than new deposits, and directing fresh savings to a Roth IRA or brokerage account restores flexibility. Still, if your state offers a generous credit—Indiana’s 20 percent credit is a prime example—keep contributing through senior year and withdraw the funds for freshman tuition. You harvest the tax perk with almost no market risk because the money is invested for only a few months.

Leave a Reply

Want to join the discussion?Feel free to contribute!