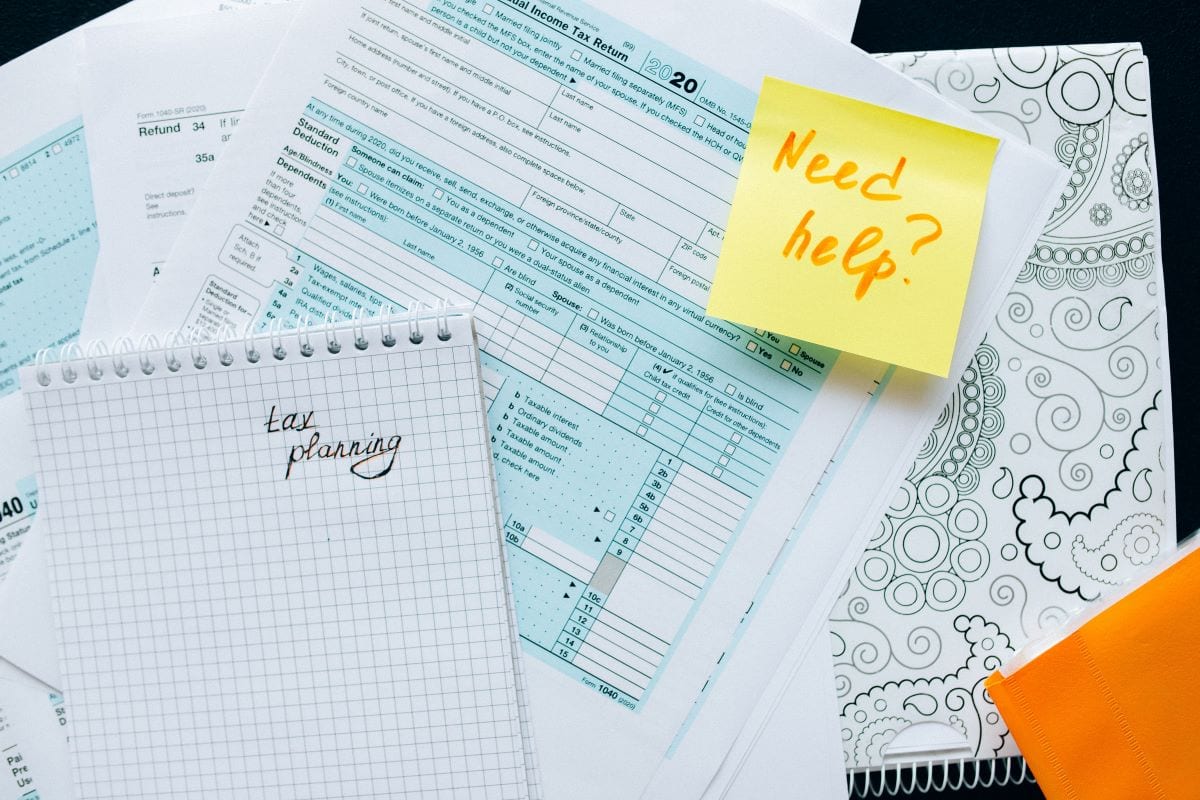

Starting a small business is a fun and exciting, but an overwhelming, task. It takes a lot of patience and practice to get the business right. From the get-go, you will encounter some mistakes or delays due to lack of understanding or not enough time. For those setting up a new business, one thing that will be on your mind is how to make a profit. In this guide, you will discover the best ways to ensure your small business can make a profit.

Ask For Help

Asking for help as a small business is key to ensure you do not do everything by yourself. You will need the advice to expand your knowledge and facilitate further development of your business. Without help, you may suffer a loss by not being able to meet customer needs or know how to market your business correctly.

There are several businesses out there that focus on helping small businesses accelerate and create revenue, such as Stephen Hourigan of Elevate Ventures. Asking for help and advice is not something to be ashamed of. There are experts out there whose job it is to offer support in order to help businesses secure a financial profit.

Make A Business Plan

Market research is the core of a business plan and a business plan is your best protection against business heartbreak.

Of the many reasons to work through a business plan, the main one is this; when you’re done, you’ll know whether or not your proposed business idea can be turned into a profitable small business. When you get your business idea right and know you can stick to the plan, you will more likely stick to targets and be on track for making a profit.

Track Your Finances Regularly

Once you have systems in place for tracking things like time, expenses, and earnings, you need to keep an eye on those things regularly. Analyzing any changes can help you determine what’s working for your business and what isn’t.

Finance tracking is a startup essential that shouldn’t be overlooked. Without accounting for your incomings and outgoings, you will not know how much your business has made or spent. You will also lose track of how much more you need to earn to make a profit.

Ensure You Offer Good Service

A small business can gain a lot from spending time serving customers and meeting their needs. No matter what type of product or service you offer, providing a great experience to customers should always be a top priority. Doing so can help you build repeat business and even gain referrals, which essentially serve as free marketing.

Do everything in your power to absolutely delight your customer. Going above and beyond to deliver an amazing customer experience increases the chance of repeat bookings, and might inspire your customer to recommend your business. These are both positive levers on the unit economic model of a business.

https://www.strategydriven.com/wp-content/uploads/company-3277947_1280.jpg8541280StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2021-03-01 20:00:052021-03-01 16:20:03How To Make A Profit As A Small Business

Managing your small business finance is crucial to maintaining stability and growing your business over the long run. From setting a budget to regularly monitoring your books, you should be proactive when it comes to managing your finances. Here is everything you need to know about managing your small business’ finance.

If you want to ensure long term growth for your company, then managing your small business’ finances is a top prerogative. From paying your employees to purchasing supplies, cash flow management is crucial to business success. Small business owners often make mistakes that, such as not separating personal and business accounts, or not paying taxes in time. Some small business owners avoid taking loans, out of fear that they’ll only be an additional financial burden.

Many of these ideas affect sustainability as well as scalability for your business. Here are ten financial management tips that will help you grow your small business:

1. Keep Your Business and Personal Account Separate

As a small business owner, starting a business bank account should be your priority. There are several benefits you gain from a business account, such as incentives, interest rates etc. that are not made available to personal bank accounts. You also ensure that financial matters related to your business is conducted through your business account only – this includes business taxes, overhead costs and paying employees.

2. Pay Yourself

Small business owners also make the mistake of not paying themselves, thinking that the extra capital can help the business. However, despite being a business owner, you also need to take care of your own expenses. Remember that you are also an employee of your business, and that means that you should be paid accordingly.

3. Loans Can Help You

Don’t be afraid of business loans. Loans can help you scale your business. Not every business owner has the capital to purchase expensive equipment, or purchase surplus supplies during a time of high demand. A business loan can help you grow your business. When done right, the return on investment is more than enough to compensate your loan as well as the interest on that loan.

4. Maintain Good Credit

This means that you need to pay your credit card bills on time, pay off any loans by the time they are due, and file your taxes on time. Good credit can help you down the line when you need to get approval for business expansions. Say you want to purchase more property, or take out a business loan. In these situations, good credit can help you get what you need to grow your business.

5. Invest in Business Growth

Your small business might benefit from better equipment, more employees, or an additional store at a good location. Investing in such opportunities helps your business to grow. At the same time, partners, lenders and even employees are more likely to see you in a positive light. This is as they see that you understand the potential of your small business, and are willing to invest in its growth.

6. Create a Budget

A budget is the easiest way to ensure that you don’t spend more than you can afford to. Every business has three costs – one time costs, recurring costs and variable costs. One time costs include equipment purchases, property purchases etc. Recurring expenses are bills, taxes, payroll, overhead costs etc. Variable expenses can come out of anywhere – such as business travel costs. Keeping these in your budget prepares you against any business disruptions.

7. Monitor Your Books

Even if you have a bookkeeper, you should also be aware of your income and expenditure. Look at your books every month so that you’re aware of your business’ cash flow.

8. Negotiate With Vendors

If your small business purchases supplies from vendors, then don’t sign any contracts immediately. Negotiate with them and see if you can bring the cost down. Ask them about grace periods and penalties in case you’re late on payments. Ensure you’ve met multiple vendors so that you know you’re getting the best deal.

9. Inspire On-time Payments for Clients

Some clients and customers don’t pay on time. If this happens to your small business, then you could find that your cash flow is being affected. Introducing incentives in the form of discounts can help you mitigate these issues. Tell customers tat if they pay on-time, they can get a 5% discount, or else they have to pay the full amount. Introduce penalties for payments that are overdue past a grace period.

10. Think Ahead

Sustainable business growth depends on a long term strategy. You need to think ahead, invest in the future and continuously grow your business in order to succeed over the long run.

It is also important for your small business to have the best business insurance. To know more, click here.

https://www.strategydriven.com/wp-content/uploads/pexels-nataliya-vaitkevich-6863254-1.jpg8001200StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2021-02-24 18:00:122021-02-24 16:22:0410 Tips for Managing Small Business Finance

Many entrepreneurs become so invested in their struggle for success that they forget a crucial reality which is business failure. Startups tend to collapse, and only a minor portion of them manage to stay afloat after a few years. But business owners – thanks to their enthusiasm for innovation – ignore the fact that cash-flow can make or break a business. If your business encounters money problems, you’ll find yourself in a financial crunch. That’s when you need to make some tough decisions about your company’s commercial future for protecting your sinking business. Are you considering packing up due to monetary complications? Don’t! Just follow these simple checks and save your brainchild.

Cash-flow leaks you should fix

A failing business is every entrepreneur’s nightmare. Many business owners incline to surrender when faced with the possibility of a near-failure. Though some accept monetary impediments as another challenge to examine the effectiveness of their business strategy. These courageous individuals manage to anticipate when the next iceberg’s coming and save the Titanic with their careful calculations. How to become one of such individuals? Here are some simple tricks that’ll help you avoid sinking:

1. Review your finances

A quarterly review of your company’s cash flow can help you apprehend any financial threat in advance. It’ll also allow you to consider your income, net profit, and expenditures. Reviewing your expenses is probably the single most important technique that may prevent bankruptcy. Moreover, avoid reaching a decision impulsively. The intuition is unreliable; hence trust data-driven decision-making. Craft your budget carefully, and then faithfully stick to it.

2. Curb needless spending

Your marketing department is the lifeblood of the whole organization. Though spending money excessively on advertisements may lead to financial downfall. Failure to arrange promotional campaigns strategically is a money-leaking tactic. If you aren’t marketing to your niche, the money’s just going down the gutter! Also, don’t waste funds designing a custom website without premature marketing research. In short, there’s no need to spend on stuff your company doesn’t need.

3. Try online tools

Modern digital tools help business managers, freelancers, and even homeowners organize their finances effectively. It’s better to purchase cost-effective online accounting software with unlimited support and expert advice. It saves your time so you can focus on other important business matters. These tech tools also make communication and collaboration among colleagues easier. You can share documents and information to enhance productivity and diminish time-wastage.

4. Focus on what’s important

Building on the previous point, spend only on projects that are making your company profitable. When Jobs returned to Apple in 1997, he discontinued the Project Newton that drained $100 million from the company. And that’s just one of the failed products canceled by him besides the Pippin and the Cube. On the other hand, your company must focus only on money-making products/services. Don’t try to bring innovation when the project lacks interest among your target audience.

5. Cut extra costs

Eliminating all discretionary expenditures must be your topmost priority. Reduce anything that seems unnecessary or mere wastage of an almost-bankrupt company’s funds. No more summer holidays or birthday parties! But that’s just an easy decision. The most challenging choice is laying off hardened employees. But, if there’s no alternative available, firing your folks can be a cruel but inevitable policy. Also, consider lowering costs on office supplies or shipping expenditures.

6. Prioritize what to pay

Your payment options vary according to their respective importance. That’s why it’s necessary to prioritize which payment must be issued first and which can be delayed. Pay the vital obligations first, not clearing, which can collapse your business. For instance, paying your employees’ salary is essential because you can’t afford their departure from the company. Paying your vendors and suppliers is your next priority. Similarly, paying taxes should be on the top of your list of expenses.

7. Reshape your fiscal plan

Rethinking your entire cash-flow management can help you avoid bankruptcy and find methods to enhance your productivity. How to perform this action? Try SWOT (strengths, weaknesses, opportunities, and threats) analysis. It’ll provide you information required for strategic planning and identifying undisclosed holes you haven’t plugged in yet. You also discover marketable opportunities – internal/external – which you’ve failed to use for maximizing the company’s profitability.

8. Strengthen your networking

Networking shouldn’t be underestimated! It’s the life-support your company sometimes needs to survive obvious failure. Your connections come to your assistance and bail you out when the ship’s sinking. Your associates help enhance business awareness and finding better clients for your organization. Make friends not just with shareholders but also with your customers. Utilize promotional gifts (pens, purses, or air fresheners) to raise your company’s profile.

9. Your customers do matter

Receive utmost feedback from your customers. Their opinions are important, and you must continue creating products that solve their problems. That’s why you need to collect information from consumers and analyze this data to modify your services. Surveys are beneficial tools for gathering information. Focus on what your consumers want, not what you wish to sell. If your services don’t resonate with the customers’ requirements, you might lose these people to your competitor.

10. Safeguard your assets

Your assets might be your last hope when your company encountered unavoidable collapse. Protect these assets since these are the lifelines you might need to save a failing business. This stuff you own can generate cash flow in the future and improve your organization’s financial situation. For instance, you can sell the machinery owned by the company or rent office space temporarily. These assets can become your much-needed backup for the business.

11. Trust your team

Your employees are your most precious asset. But it’s your responsibility to ensure their correct utilization. Employees who’re working just for the paycheck might not be the right choice for your company. You need to connect with them and ascertain that they understand your business model. Your workers must be dedicated individuals who’ve committed themselves to success. Train them to become more efficient and listen to their recommendations to promote communication.

12. Cherish the risk

Entrepreneurship thrives on risks and challenges. Some business owners prefer playing it safe during a time of crisis. In reality, avoiding risks may diminish your productivity and tamper with your innovative essence. Making brave decisions is often the route to save your failing company. When Private White decided to release branded products, they faced the responsibility of handling inventory and marketing. But this decision ultimately contributed to their growth and popularity.

Conclusion

As an entrepreneur, you might’ve speculated the most dominant reason for business failure. Here’s what the experts agreed upon after a careful investigation. According to the U.S. Bank, 82% of small businesses collapse due to poor cash-flow mismanagement! No wonder there’s an 80% chance that your company’s toast after two decades of service. Moreover, startups crumple since around 80% of them begin with insufficient funds or haven’t created a well-established business strategy. In short, money problems can rupture your smooth-sailing vessel and leave you a veteran of financial bankruptcy. So, avoid financial losses and develop a fiscal awakening. Follow our suggestions and avoid failure.

https://www.strategydriven.com/wp-content/uploads/pexels-karolina-grabowska-4386472.jpg8001200StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2021-02-23 16:00:112021-02-23 15:18:13Is Your Business Sinking? 12 Holes You Need To Plug

Various studies conducted show that relevant advice availed to individuals on pensions is relatively low. Pension plans are a saving platform for retirement where employers contribute funds towards their employee’s retirement. There are two types of pension plans, which include the defined benefit and the defined contribution plan. The final salary pension is a source of a stable savings plan, a source of income paid to pension holders after retirement. Mis-sold Pensions lead to considerable losses to an individual pension fund. When one has poor financial advice, they transfer their saved money and invest in unstable business ventures. Some companies and individuals offer pension holders services when they want to make claims due to financial losses. The court provides relatively low claims, but it is the most efficient tool as it holds all the parties involved accountable. Private practitioners like lawyers offer quality services, and they charge higher amounts of money on their services. Before committing to any pension plan, ensure that it meets your needs and contributions are not a financial burden. In case a pension holder dies, the family members are given the accrued benefits.

Mis Sold Pension Plans

There are various types of the mis-sold pension plans, including the SIPP, final salary transfers,SASS, and OPS. The self-invested pension plans give the pension holders control over their pension funds, and they are a high-risk investment that may lead to massive losses. They fail to provide enough attention to the service provider on the quality of information delivered. Complaints are made against the pension provider and the recommended financial advisors. In case of a mis-sell, individuals are allowed to make claims, and when approved, one is compensated. The final salary transfers involve employers’ contribution of a certain amount of money towards a pension plan for the employees. It is considered to be a secure saving plan and gives a guaranteed benefit as losing pension funds is a rare occasion. If advised to transfer to another kind of pension plan without your due diligence, you are entitled to make compensation claims. The small self-administered schemes are unregulated, and they are high-risk investments. In any case, a regulated financial officer encourages a transfer to the pension plan; you can directly ask for compensation. The occupational pension schemes are created by employers who enable employees to save for their retirement and are regulated.

Claims in Mis-Sold Pensions

Some financial advisors recommended by the pension providers give misleading advice, which leads to financial losses. In such situations, individuals are encouraged to make claims through the various platforms available. One can directly involve the courts or the financial service. The provided financial services are cheap, and their decisions can only be challenged in a court of law. The claiming process is slow due to inadequate financing making their services inefficient, and huge claims put pressure on the systems. Private practitioners like companies have experienced personnel who directly engage you in the claiming process by making sure information is available on any proceedings. Individuals can make claims to the pension providers if they lack enough capital to hire the relevant service providers.

Signs of a Mis-Sold Pension

There are stipulated practice codes that require financial advice to offer excellent and relevant financial advice about the available pension plans, including the associated benefits and disadvantages. The pension plan should cover all the individuals’ needs and have high stability to prevent losses. The provided information ensures that decisions made are informed and limit cases of claiming compensation. To identify if the financial advisor has misguided, you have proof showing that the information offered is biased and is not exhaustive on all the products available in the market. Financial losses are substantial proof that results from a lack of enough information on the various business ventures resulting in profits. Financial advisors may advise on transferring stable pension plans to highly risky plans that attract losses if not well managed. Individual research is recommended from the various sources of information and seeking relevant advice from the private financial practitioners on the pertinent pensions which meet a person’s needs without compromising its security.

Pension Transfers

There is a specified period to make any claim of a mis-sold pension plan; if the claim is not completed, then compensation becomes impossible. There are various set financial services that help complainants receive fair judgments and handle the policyholders’ pension complaints. The claiming process takes some time for a solutions agreement, and it does not mean that the complainant will not receive compensation. In case one feels that the pensions they have do not meet their needs, individuals are allowed to make transfers, which eventually suits their needs. Individuals with final salary transfers may wish to shift to defined contribution plans if they are willing to venture into the high-risk plans and make the relevant business decisions to grow their pension funds actively. Transfer from the high-risk pension to the defined plans ensures security and a guaranteed income source in the future when one retires. The significant benefit of pension plans is they are a savings plan, and when the pension holder dies, their immediate family or beneficiary directly receives the benefits from the pension.

Taxation and Time Taken to Make a Claim

In most cases, taxation of the pension funds is not allowed making it an efficient saving plan. The government offers social security to the more senior members of society by providing untaxed amounts of money to cater to their daily needs. The time it takes to access the claim depends on how complex the case is and all parties’ availability to appear in the proceedings. Some cases take years to solve, and others take months for a conclusion to be made. Private practitioners take less time to make relevant claims as they follow a stipulated time frame to ensure their clients are satisfied. The earlier you predict a mis-sell and report the matter, the quicker the solutions are availed to the stakeholders.

In conclusion, a pension plan is a saving plan that mostly pays off when pension holders retire. Relevant financial advice is required in choosing the appropriate pension plan which meets persons` needs. When you realize you have a miss-sell, start to make a claim immediately to use a short time frame to wait for decisions. One can make a pension transfer if their current pension plan is inadequate to their needs. Ensure you have the relevant information when choosing any pension plan.

https://www.strategydriven.com/wp-content/uploads/pexels-pixabay-534216.jpg6571200StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2021-02-16 16:00:072021-02-16 13:35:37Do You Have Relevant Information on Pensions?

Most new entrepreneurs are at several particular and distinct disadvantages to the established players in their fields.

Perhaps first and foremost, giant established companies will have vast financial resources at their disposal, which can be used to pursue all manner of different innovations and campaigns, while also allowing them to more easily and effectively absorb losses.

For a new entrepreneur, there are all sorts of different things that should be taken into account when it comes to following the most productive path forward. Figuring out how best to avoid wasting money is a key priority.

Here are some tips on how to avoid wasting money as a new entrepreneur

Don’t invest in countless training materials, but learn “on-the-job”

There is a very large industry out there focused on selling books, instructional DVDs, motivational speeches, and more technically-focused “training materials” and “mentorship programs,” for entrepreneurs in general.

While some of these may certainly be helpful in particular contexts, the truth is that, in the majority of cases, these training courses, books, and so on, are unlikely to make much of a difference to your professional life. What they likely will do, though, is to drain your bank balance.

For the most part, the best way to learn how to do things as an entrepreneur is through “on-the-job experience.” Both your successes and your missteps and mistakes will give you a lot of insight about where you need to make adjustments versus staying on the current path.

Invest extra where it counts, but don’t fall for the idea that higher prices always reflect superior outcomes

In a professional context, there are always going to be areas where investing extra money results in a higher overall quality of service, and superior outcomes overall, that can significantly enhance the experience of your customers and improve the prospects of your business.

At the same time, however, there are also going to be many areas where spending a lot of money will not make much difference in outcome compared to spending a more moderate amount of money.

An important art to master is figuring out where that extra investment of money will really count, and where it won’t. The cheapest UPS domestic shipping rates are likely to get the job done well, in many cases.

Work on a focused number of things at a time, instead of trying to cover all the bases

The more you try to “do it all” as an entrepreneur, and to “cover all bases,” the less progress you are likely to make on any one thing at a time, and the less efficient you are likely to be with your money, as well.

By focusing on a limited number of things at a time, you can make more impact with your money, and can also keep your business moving in a more coherent direction.

While you can certainly branch out and add new features to your business over time, trying to do too much at once is often a road to self sabotage.

https://www.strategydriven.com/wp-content/uploads/word-image-85.jpeg12801920StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2021-02-12 09:00:282021-02-12 22:00:213 Tips to Avoid Wasting Money As a New Entrepreneur

Starting a small business is a fun and exciting, but an overwhelming, task. It takes a lot of patience and practice to get the business right. From the get-go, you will encounter some mistakes or delays due to lack of understanding or not enough time. For those setting up a new business, one thing that will be on your mind is how to make a profit. In this guide, you will discover the best ways to ensure your small business can make a profit.

Starting a small business is a fun and exciting, but an overwhelming, task. It takes a lot of patience and practice to get the business right. From the get-go, you will encounter some mistakes or delays due to lack of understanding or not enough time. For those setting up a new business, one thing that will be on your mind is how to make a profit. In this guide, you will discover the best ways to ensure your small business can make a profit.