Running a small business in Indiana involves making decisions that affect profitability, compliance, and long-term growth. While many entrepreneurs confidently manage sales, operations, and customer relationships, tax preparation is an area where even small mistakes can have significant financial consequences. Filing errors, missed deductions, inaccurate payroll reporting, or overlooked tax law changes can result in penalties, interest charges, and unnecessary stress.

Professional tax preparation helps reduce these risks by combining technical expertise with ongoing financial guidance. Rather than simply completing an annual tax return, experienced tax professionals help business owners maintain compliance, improve recordkeeping, and make informed financial decisions throughout the year. For small businesses, this proactive approach often proves far more valuable than attempting to handle increasingly complex tax requirements alone.

Why Professional Tax Preparation Is a Smart Risk Management Strategy

Tax preparation is about much more than meeting a filing deadline. Every business decision, from hiring employees to purchasing equipment, can have tax implications. Professional guidance helps identify potential issues early, reducing the likelihood of costly mistakes while improving overall financial organization.

Here are some of the biggest ways professional tax preparation helps protect small business owners.

1. Audit Red Flags

No tax preparer can promise that a business will never be audited, but professionally prepared tax returns are generally more accurate, consistent, and supported by proper documentation.

Certain filing issues may attract additional scrutiny, including unusually high deductions, inconsistent reporting, mathematical errors, or incomplete financial records. A tax professional reviews returns carefully before submission, ensuring deductions are properly documented and reported according to current tax regulations.

They also help business owners maintain organized records throughout the year, making it easier to respond if tax authorities request additional information. Well-prepared documentation not only simplifies the audit process but also demonstrates that reasonable care was taken when preparing the return.

2. Prevent Costly Filing Errors

Tax laws contain countless rules governing depreciation, business expenses, payroll taxes, estimated tax payments, retirement contributions, and industry-specific deductions. Small errors in any of these areas can result in penalties, delayed refunds, amended returns, or additional tax liabilities.

Professional tax preparers help eliminate many of the mistakes commonly made by business owners preparing returns themselves, including:

Incorrect deduction calculations.

Missed business expense opportunities.

Reporting income inaccurately.

Applying the wrong depreciation methods.

Filing incorrect business tax forms.

The cost of correcting tax errors often exceeds the cost of professional preparation, making accuracy an important investment rather than simply an expense.

3. Stay Compliant With Changing Tax Laws

Tax legislation changes regularly, and keeping up with those changes can be difficult while running a business. Federal regulations, state tax requirements, filing deadlines, deduction limits, and reporting obligations may all change from year to year.

Professional tax preparers continually monitor these developments and apply current regulations when preparing returns. They can also explain how legislative changes may affect business decisions throughout the year rather than waiting until tax season arrives.

Combining official guidance with professional expertise helps businesses remain compliant while reducing the risk of avoidable penalties.

4. Avoid Payroll and Worker Classification Mistakes

As businesses grow, payroll responsibilities become increasingly complex. Employers must properly classify workers, calculate payroll taxes accurately, and meet reporting deadlines throughout the year.

Misclassifying an employee as an independent contractor, for example, can lead to back taxes, penalties, interest, and additional reporting obligations. Payroll calculation errors may also trigger government inquiries or require corrected filings.

Professional tax advisors help businesses:

Classify workers correctly.

Meet payroll tax deadlines.

Calculate withholdings accurately.

Maintain organized payroll records.

Comply with federal and state employment tax requirements.

Addressing these issues proactively is significantly easier than correcting them after an audit or regulatory review.

5. Benefit From Year-Round Tax Planning

The greatest value of professional tax preparation often comes outside of tax season. Ongoing tax planning allows businesses to make financial decisions with future tax consequences in mind instead of reacting after the year has already ended.

Regular planning can help businesses improve cash flow, estimate quarterly tax payments more accurately, evaluate equipment purchases, maximize available deductions, and determine whether their current business structure remains the most tax-efficient option.

For many business owners, relying on trusted tax preparation Garrett, IN services helps ensure accurate tax filing while staying ahead of compliance requirements.

Arise Tax works with small businesses throughout Garrett and the surrounding communities, providing tax preparation and advisory services designed to help business owners stay compliant while making informed financial decisions throughout the year.

6. Receive Professional Support During an Audit

Even businesses that maintain excellent records may occasionally receive notices requesting additional documentation or clarification. Without professional assistance, responding to these requests can be stressful and time-consuming.

Experienced tax professionals understand what tax authorities require and can help organize financial records, prepare supporting documentation, and communicate throughout the review process. Their familiarity with tax procedures allows business owners to respond more efficiently while avoiding unnecessary mistakes.

Having professional support also provides peace of mind, particularly for owners who may not be familiar with complex tax regulations or audit procedures.

Choosing the Right Tax Professional

Not every tax preparer offers the same level of expertise for small businesses. Beyond preparing returns accurately, a qualified advisor should understand your industry, business structure, and long-term financial goals.

When evaluating a tax professional, consider whether they:

Have experience working with businesses similar to yours.

Offer year-round advisory services rather than seasonal filing only.

Stay current with federal and state tax law changes.

Provide assistance if questions or audits arise.

Communicate clearly about tax planning opportunities throughout the year.

A long-term relationship with a knowledgeable tax professional often provides greater value than simply hiring someone to complete an annual return.

Conclusion

Professional tax preparation reduces risk in ways that extend far beyond filing an accurate return. By preventing costly errors, reducing audit risks, maintaining compliance with changing regulations, and providing year-round planning, experienced tax professionals help small business owners make more confident financial decisions.

Rather than spending valuable time navigating complex tax rules, business owners can focus on growing their companies while knowing their tax obligations are being managed accurately and proactively. Over time, that combination of compliance, planning, and professional guidance becomes an important part of building a stronger and more resilient business.

https://www.strategydriven.com/wp-content/uploads/IMG_2182.jpeg8571500StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2026-06-29 15:04:222026-06-29 15:04:22How Professional Tax Preparation Reduces Risk for Small Business Owners

A developing company faces more and more tax issues as it grows. New markets, new employees, merger & acquisitions, restructuring, or financing may require the attention of tax advisers. This challenge is universal regardless of the country. While a business may operate in Australia, the USA, the UK, Singapore, or Canada, tax governance becomes essential for scaling up even though there are differences in regulations, thresholds, and procedures from one country to another.

Nevertheless, many businesses are mostly focused on the growth of revenue and operations and neglect tax issues until there is a problem. However, a proactive attitude to tax compliance could help to lower risk, increase the effectiveness of the business, and avoid future disputes with the authorities.

To illustrate the importance of this problem, let us discuss the Australian experience of tax compliance, when the Tax Office actively works to ensure that all the organizations meet their obligations and when the tax disputes happen quite fast as soon as a business goes beyond its initial phase of development.

More Complexities as the Business Grows Up

As the company expands, it not only files taxes on time, but also encounters various tax problems connected with foreign expansion, acquisition, financing, incentives, and restructuring. Inability to deal with all these matters might bring extra tax liabilities, fines, and tax controversies.

Australian experience illustrates this process well. For instance, in recent years, there have been numerous tax disputes of large companies concerning their international structures, transfer pricing policies, and significant corporate transactions. What is interesting about these cases is that the main reason for conflict was not the misconduct of the business but merely the complexity of operating across the borders, structures, and transactions without sufficient specialized advice.

The same thing happens in other countries as well. A business that wants to expand its presence in Singapore from the UK or a company from Canada acquiring a subsidiary in the USA is in the same situation – different in details but identical in its essence.

Tax Governance Is Part of Good Strategy

Today, good tax governance is not a job for the finance department anymore. It requires business leaders to think of tax implications of their strategic decisions, including investments, expansions, and organizational changes. This kind of approach will help the business avoid uncertainty and make informed decisions.

The regulators become aware of this idea as well. Thus, Australian tax authorities have started to pay more attention to the corporate tax governance framework by requiring large companies to demonstrate that tax risk is actively managed at the highest management level and not at the operational one.

Those companies that have some documentation about tax governance processes, escalation policy in case of uncertain positions, and board of directors awareness of the tax risk tend to cope with the questions better since they could prove that their decisions were carefully considered.

However, this process is also relevant to mid-size businesses during their first acquisitions, overseas hiring, and organizational changes since tax considerations were neglected from the very beginning of the strategic process.

Do Not Wait Until Your Company Needs an Audit or Tax Dispute

A lot of companies consult a tax lawyer after receiving an audit notice or becoming entangled in the dispute. However, taking into account potential tax risks and problems in advance might help the company to avoid them.

Usually, when an organization receives a notice of audit, it means that it is already too late to take necessary actions. Some positions were made, some transactions were concluded, some documents were collected that might contradict a later position. Therefore, seeking professional advice at the planning stage allows the business to test its assumptions, make corrections, and collect all the documentation.

Companies conducting some significant transactions, facing some tax problems, or carrying out restructures could benefit from consulting experienced tax lawyers. This kind of advice is especially useful in countries like Australia, where the tax controversy has become a separate practice of law with the specialized practitioners familiar with both the technical aspects of tax position and the approaches of the regulators.

Choosing a Proper Tax Adviser

Different law firms specialize in different fields. Therefore, before consulting a tax adviser, the company should examine its practice and experience and make sure that it is suitable for the organization. The majority of commercial firms provide assistance with tax, corporate transactions, dispute resolution, banking and finance, employment, and regulation matters, thus helping a business at any stage of its development.

Moreover, if the organization has some cross-border operations, the company should choose a firm that has enough experience in working in the particular countries and not the firm with a general commercial practice. Firms with tax controversy capabilities, experience in international tax laws, and negotiation with revenue authorities would have much better chances to help a business solve its problems or avoid them in advance than a generalist practice.

Conclusion

Development brings some legal and tax responsibilities to the business. Considering tax issues in advance and consulting the tax lawyers will help the business avoid risks and make better decisions.

The Australian experience demonstrates the importance of this approach: companies that include tax considerations in their strategic plans have a better opportunity to cope with the disputes and, most of the time, to avoid them. No matter what country the company operates in, proactive tax planning is always better than reaction to the problems.

https://www.strategydriven.com/wp-content/uploads/IMG_2181.jpeg10251500StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2026-06-25 13:33:342026-06-25 13:33:34Why Growing Businesses Should Not Wait Until Their Tax Issues Turn Into Legal Issues

Deciding to pursue debt relief is a big step — one that comes with real consequences, meaningful benefits, and a fair amount of complexity. Yet many business owners walk into the process without a clear picture of what it actually involves, what it will cost them, or what the realistic outcomes look like.

In a city like Washington, D.C. — where small businesses operate in a high-cost environment shaped by federal policy, shifting government contracts, and one of the most competitive commercial real estate markets in the country — financial pressure on business owners is rarely simple. The debt relief landscape is equally layered.

Before you take any formal steps, here are seven things every business owner should genuinely understand about the debt relief process — the kind of grounded, honest perspective that saves you from costly surprises.

1. Not All Debt Relief Options Are the Same

“Debt relief” is an umbrella term that covers several very different approaches — and they don’t all lead to the same place. Debt consolidation merges multiple obligations into a single loan, usually at a lower interest rate. Debt settlement involves negotiating with creditors to accept less than the full amount owed. A structured repayment plan restructures the timeline without reducing the principal. Bankruptcy, at the far end of the spectrum, provides a legal discharge of qualifying debts.

Each option has different eligibility criteria, credit implications, timelines, and costs. What works for one business may be entirely wrong for another — even in a similar financial position. Understanding this range upfront prevents you from pursuing a path that doesn’t fit your actual situation.

The first conversation with any professional should help you identify which category you actually belong in — not push you toward a predetermined product.

2. Your Credit Will Be Affected — Plan for It

Most forms of business debt relief carry some credit impact. Settlement programs typically require accounts to go past due before negotiations begin — which shows up on credit reports. Consolidation loans affect your utilisation ratio. Bankruptcy, depending on the type, remains on a credit profile for seven to ten years.

This doesn’t mean debt relief is the wrong choice. For many businesses, the short-term credit hit is a reasonable trade for the long-term stability that comes from resolving unmanageable debt. But it does mean you should know what’s coming — so you can plan around it rather than be surprised by it.

Questions worth asking before you start:

Will I need business financing in the next 12 to 24 months?

Do any key contracts or leases depend on a minimum credit rating?

How long will recovery take after the program ends?

3. Timing Changes What’s Possible

The window of available options narrows as a debt situation ages. Early in a financial difficulty — when accounts are still current but cash flow is clearly unsustainable — a business has considerably more negotiating leverage than it does six months later when accounts are in collections and legal action is looming.

Creditors are generally more willing to negotiate modified terms before they’ve classified a debt as a loss. Once an account has been written off and sold to a collections agency, the flexibility shrinks and the conversation becomes more adversarial.

Acting earlier doesn’t mean panic — it means preserving options. A proactive conversation with a specialist when the situation is still developing is almost always more productive than a reactive one after it has deteriorated.

4. Secured and Unsecured Debt Behave Differently

This distinction matters enormously and is frequently misunderstood. Unsecured debts — credit cards, lines of credit, supplier invoices — have no collateral attached and are generally more negotiable. Secured debts — mortgages, vehicle loans, equipment financing — are backed by a physical asset, which changes both the risk and the leverage in any negotiation.

Attempting to include secured debts in a settlement program without understanding the implications can result in asset repossession or foreclosure. Any debt relief strategy needs to be structured around this distinction from the outset — with a clear assessment of which debts can be negotiated and which carry collateral risk.

A qualified professional will categorise your obligations before recommending anything — this is a foundational step, not a formality.

5. Who You Work With Matters As Much As the Plan

The debt relief industry is not uniformly regulated, and not every company offering these services operates with the same standards. Some charge high upfront fees before delivering any results. Others use aggressive sales tactics that push businesses into programs that don’t fit. A few simply take fees and produce nothing of value.

Business owners in the capital region researching their options and looking into debt relief Washington, District of Columbia services should prioritise providers who are transparent about fees, accredited through recognised industry bodies, and willing to explain the full process before any agreement is signed.

Firms such as US National Credit Solutions operate with clear disclosures and works to match businesses with programs suited to their actual financial profile — not the most profitable option for the firm.

6. The Numbers Need to Be Fully Honest

Debt relief works best when it’s built on accurate, complete financial information. That means a full accounting of every obligation — not just the ones keeping you up at night. Business owners sometimes understate what they owe, omit debts they expect to resolve independently, or overestimate incoming revenue. Any of these gaps can result in a plan that looks workable on paper but fails in practice.

Before your first consultation, gather the following:

A complete list of all business debts with current balances and interest rates

Three to six months of business bank statements

A realistic monthly cash flow summary — income and all expenses

Details of any personal guarantees tied to business debt

Going in with complete information isn’t just helpful — it’s what makes the difference between a plan that holds and one that unravels after the first unexpected expense.

7. Relief Is a Starting Point, Not a Finish Line

Completing a debt relief program is a genuine achievement — but it doesn’t automatically resolve the conditions that created the debt in the first place. Without addressing the underlying causes — whether that’s an unsustainable pricing model, high overhead, poor receivables management, or seasonal cash flow gaps — the same pressures can resurface.

According to the Federal Deposit Insurance Corporation (FDIC), businesses that pair debt resolution with basic financial management improvements — including cash flow planning and disciplined expense tracking — are significantly more likely to maintain financial stability in the years following a relief program.

The most valuable debt relief programs don’t just negotiate balances — they leave you with a clearer understanding of your finances and a realistic plan for keeping them that way going forward.

Conclusion

Debt relief done well is a powerful tool. It can reduce what you owe, restructure impossible payment terms, stop creditor pressure, and give a struggling business the breathing room it needs to recover. But it works best when you enter the process with clear expectations, honest numbers, and the right professional in your corner.

The seven points above aren’t meant to discourage anyone from seeking help — quite the opposite. They’re meant to make sure that when you do take that step, you take it with your eyes open and your position well prepared.

Understanding the process is the first act of taking back control of it.

https://www.strategydriven.com/wp-content/uploads/IMG_2125-scaled.jpeg20482560StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2026-06-15 12:57:102026-06-15 12:57:10What Every Business Owner Should Understand Before Seeking Debt Relief

Brisbane is expanding rapidly. With the population surging and major infrastructure projects ramping up across the city, the opportunities for small businesses are obvious. But growth eats cash. Whether you are taking on a larger warehouse in Richlands, upgrading your software systems, or hiring a new crew to handle government contracts, you need money behind you.

Scaling a business without adequate capital usually leads to burnout or failure. Bank loans used to be the default answer. You would take your business plan to the local branch manager and wait six weeks for a decision. That model is mostly dead. Traditional banks are often too slow and their lending criteria too rigid for fast moving operators. Business owners have to look at the whole board to fund their next phase of growth. Here is a look at the commercial funding mechanisms actually working in the market right now.

Equipment and Asset Finance

If your growth strategy relies on heavy machinery, commercial vehicles, or specialised equipment, paying cash upfront is usually a mistake. Emptying your bank account to buy a physical asset leaves you vulnerable to everyday cash flow gaps.

Asset finance lets you acquire the equipment immediately while spreading the cost over its useful life. The machinery itself acts as the security for the loan. This keeps your working capital intact. For transport and logistics operators working out of Acacia Ridge or the Port, putting the right vehicles on the road quickly is the entire game. If you are looking at truck finance Brisbane, you will find non bank lenders who deal exclusively in the transport sector. They know the commercial lifespan of a prime mover and will structure terms and balloon payments that match your actual revenue cycles. You get the equipment to generate income right away while paying it off in predictable chunks.

Unsecured Business Loans for Speed

Sometimes you do not have a hard asset to secure a loan against. You just need a fast injection of cash to fund a marketing push, buy bulk inventory ahead of peak season, or cover wages while waiting for a major contract to commence.

Unsecured lending has evolved heavily over the last few years. The main trade off is straightforward. You pay a higher interest rate because the lender carries more risk. What you get in return is speed. Many alternative lenders can approve and fund a loan in 24 hours just by connecting to your Xero or MYOB account and reviewing your recent bank statements. For a retail or hospitality venue wanting to renovate quickly, the fast access to funds easily outweighs the higher cost of capital. The key is knowing exactly how the funds will generate a return to cover the debt.

Invoice Financing for B2B Operations

Waiting 30 to 60 days for clients to pay their invoices is a massive handbrake on growth. It forces you to act as a free credit facility for your larger clients.

Invoice finance changes this dynamic. It allows you to access up to 80 percent of the value of your outstanding invoices almost immediately. The lender advances you the cash upfront. When your client finally pays the invoice, the lender passes on the remaining 20 percent minus their facility fee.

This effectively turns your accounts receivable into liquid cash. You are not taking on debt in the traditional sense. You are just paying a premium to access your own money faster. For manufacturing, wholesale, and labour hire businesses in Brisbane, this structure is highly effective for smoothing out lumpy cash flow.

Overdrafts and Lines of Credit

A business line of credit works basically like a large credit card. You are approved for a set limit and you only pay interest on the funds you actually draw down.

This is one of the most practical tools for managing seasonal fluctuations. If you run a service business, having a revolving line of credit sits in the background as a safety net. You draw on it to pay suppliers when cash is tight and pay it back down to zero when your major invoices clear.

Getting a facility set up requires strong historical finances. Banks and alternative lenders will look closely at your trading history and ATO compliance. Once it is established, it requires very little daily management.

Alternative Asset Liquidity

When credit markets tighten, traditional lenders pull back their risk appetite. Business owners often have to look at their own balance sheets and personal holdings to fund their next strategic move. This is where alternative and physical assets come into play.

Some founders choose to liquidate or borrow against physical investments to inject cash into their business quickly without jumping through endless banking hoops. I have seen founders quietly turn to Brisbane bullion dealers to offload company owned or personal precious metal reserves when they need immediate capital. Gold and silver are highly liquid. Converting them to cash can bridge a sudden funding gap much faster than waiting for a commercial property refinance to clear. It is a niche approach but highly effective for those who hold physical reserves.

Private Equity and Angel Investment

Taking on debt is not the only way to fund growth. Bringing in outside investors exchanges a percentage of your company equity for cash.

Brisbane has an active angel investor network. Selling equity means you do not have to worry about monthly loan repayments draining your cash flow while you try to build the business. The money can be put entirely toward product development, marketing, and scaling the team.

The downside is the long term cost. Giving up 15 percent of your company might solve your cash problem today, but that 15 percent could be worth millions in five years. You also give up a degree of control. Investors will want a say in how the business is run and will expect regular reporting on your metrics.

Structuring Your Debt Correctly

There is no single correct way to fund a company. The best operators use a strategic mix of these tools. They might use asset finance for their fleet, an unsecured loan for a one off inventory purchase, and a line of credit for seasonal wage management.

The goal is always to match the type of finance to the purpose of the funds.

Do not use a short term unsecured loan to buy an asset you will use for a decade.

Do not tie up your family home as security just to cover a temporary cash flow dip.

Get the funding structure right from the start. If you mix short term debt with long term assets, you put the business under immediate repayment pressure. Good financial hygiene means sitting down with your accountant or commercial broker and mapping out exactly what the capital is for, how long it will take to generate a return, and what happens if the market turns.

Debt is just a tool. It only becomes a burden when you use the wrong product for the job.

https://www.strategydriven.com/wp-content/uploads/IMG_2086.jpeg10011500StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2026-06-03 21:40:272026-06-03 21:40:27What Financing Options Help Small Businesses Grow Faster in Brisbane?

The Evolution of Commercial Real Estate Investment

For many businesses, a commercial warehouse is more than just a building; it’s the operational core. In May 2026, efficient logistics and scalable space are essential for staying competitive. Securing the right commercial warehouse for lease is therefore crucial for sustained growth.

We understand that navigating this complex real estate sector can be challenging. This guide aims to simplify the process and help you make informed decisions. We will cover what commercial warehouses are, where to find them, and how to understand rental rates and sizes. We will also discuss different space types, key evaluation factors, and relevant market trends. Our focus will be on helping you find the ideal setup, including adaptable warehouse spaces, to meet your business needs.

The commercial real estate landscape in May 2026 is a dynamic ecosystem, continuously reshaped by global economic shifts, technological advancements, and evolving consumer behaviors. We observe a market characterized by both robust demand in specific sectors and strategic adaptation in others. Market liquidity remains strong for high-quality assets, particularly those supporting e-commerce and logistics. Urban expansion continues to drive demand for commercial spaces, but often with a renewed focus on mixed-use developments that integrate living, working, and retail environments.

Industrial demand, especially for warehousing and distribution centers, has seen unprecedented growth, largely fueled by the persistent rise of e-commerce. Businesses are increasingly seeking strategically located facilities to optimize their supply chains and meet ever-tightening delivery expectations. This trend is evident in major logistics hubs across North America. For instance, regions like Burnaby, Surrey, and Vancouver in Canada continue to experience high demand for industrial space, with limited inventory driving up rental rates. Similarly, emerging markets and established logistical corridors in the United States, such as those found in Alabama, are witnessing significant investment and development in the industrial sector. This sustained interest underscores the critical role that efficient storage and distribution play in the modern economy.

Diversification through Commercial Real Estate Investment

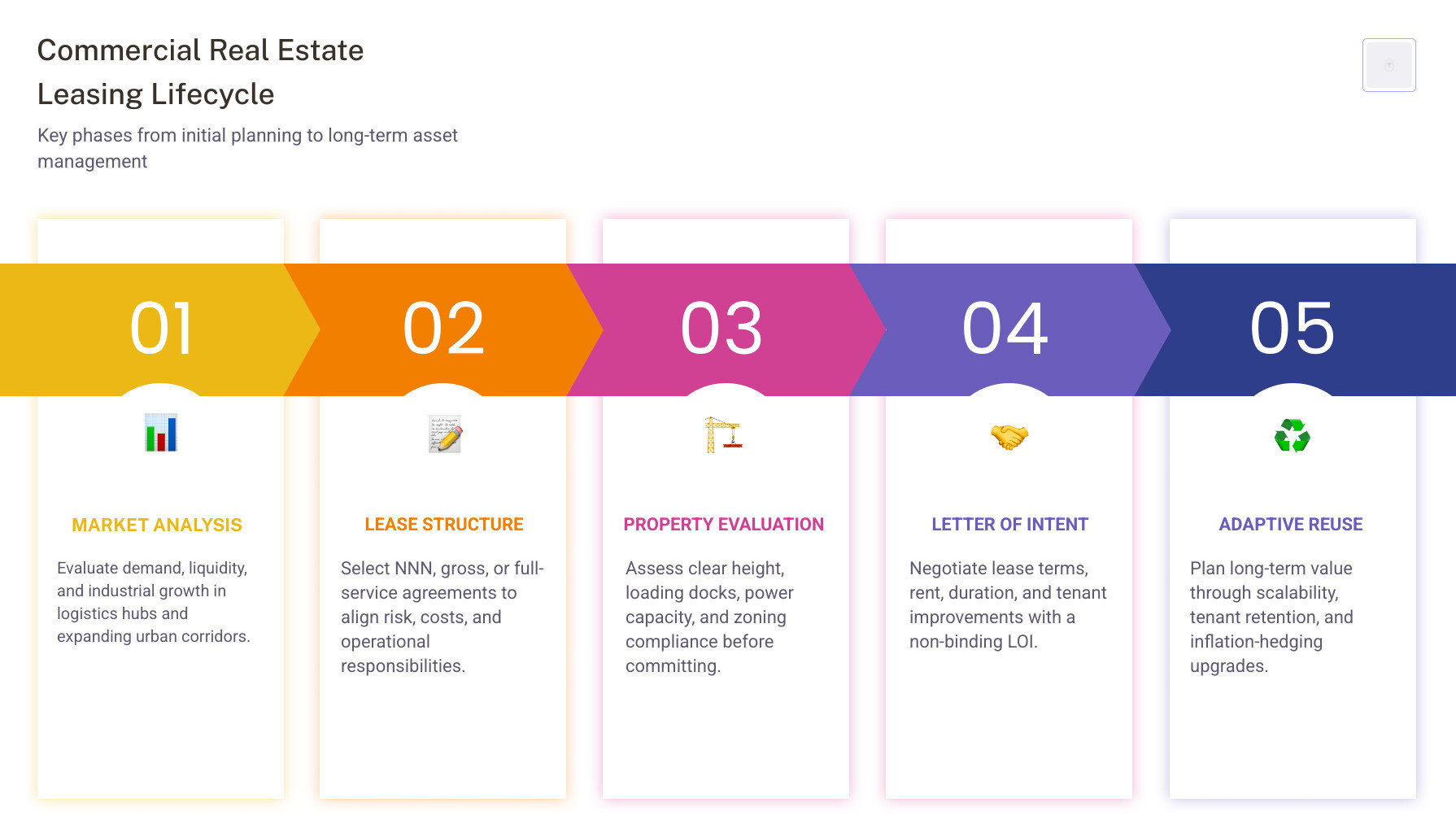

Investing in commercial real estate offers a compelling avenue for portfolio diversification, providing a tangible asset class that can act as a hedge against market volatility. One of the primary benefits is risk mitigation, as commercial properties often exhibit less correlation with traditional stock and bond markets. Understanding the various lease structures is paramount for investors and tenants alike, as they directly impact risk and responsibility.

Triple Net (NNN) leases, for example, place the burden of property taxes, insurance, and maintenance costs squarely on the tenant, offering landlords a more predictable and passive income stream. This structure is particularly attractive for single-tenant industrial properties where the tenant has significant control over the premises. In contrast, Gross leases typically include all operating expenses in a single rental payment, simplifying tenants’ budgeting but requiring landlords to manage and absorb these fluctuating costs. Full-service structures, often found in multi-tenant office buildings, bundle nearly all expenses, including utilities and janitorial services, into the rent, providing tenants with a comprehensive, worry-free solution. Each of these structures offers distinct advantages and disadvantages, influencing capital appreciation and operational overhead for both parties. Strategic selection of lease type is crucial for aligning with investment goals and operational needs.

Long-term Value in Commercial Real Estate Investment

The long-term value proposition of commercial real estate investment is rooted in several key factors that contribute to sustained returns and asset appreciation. Tenant retention is a critical element; a stable tenant base reduces vacancy rates and turnover costs, ensuring consistent income. Properties that offer modern amenities, strategic locations, and flexible layouts are more likely to attract and retain high-quality tenants.

Adaptive reuse is another powerful strategy for enhancing long-term value. Transforming older, underutilized properties into modern, functional spaces – such as converting former manufacturing plants into creative office hubs or industrial flex spaces – can unlock significant value and extend the economic life of an asset. Scalability, the ability to expand or reconfigure space to meet evolving business needs, is increasingly important, particularly for industrial and flex properties. This inherent flexibility makes properties more attractive to a broader range of tenants over time.

Furthermore, commercial real estate often serves as an effective inflation hedge. As inflation rises, property values and rental income tend to increase, preserving purchasing power and enhancing returns. Finally, institutional-grade assets, characterized by their size, quality, and strong tenant rosters, are particularly sought after by large investors for their stability and long-term growth potential. These factors collectively underscore why commercial real estate, when strategically managed, can be a cornerstone of a resilient investment portfolio.

Essential Criteria for Selecting a Commercial Warehouse for Lease

When searching for a commercial warehouse for lease, a meticulous evaluation of essential criteria is paramount to ensure the space aligns perfectly with your operational demands. Beyond the basic square footage, critical physical attributes dictate a warehouse’s suitability. Clear height, for instance, refers to the usable vertical space from the floor to the lowest obstruction (such as support beams or sprinklers), which directly impacts storage capacity and the ability to operate specialized equipment, such as forklifts. Adequate loading docks, including their number, type (dock-high or grade-level), and configuration, are vital for efficient inbound and outbound logistics. The power capacity, measured in amperage and voltage, must meet your machinery and operational requirements, especially for manufacturing or heavy industrial uses.

Zoning regulations are non-negotiable; they dictate what types of businesses and activities are permitted in a specific area, influencing everything from operating hours to noise levels and environmental considerations. Understanding these regulations early can prevent costly delays or legal issues. The process of securing a lease typically begins with a Letter of Intent (LOI), a non-binding document outlining the proposed lease terms, including rent, lease duration, and tenant improvements. This initial step allows for negotiation before a formal lease agreement is drafted. A thorough property evaluation, encompassing structural integrity, utility infrastructure, and environmental assessments, is crucial before committing to a lease. For businesses seeking highly customizable solutions, exploring adaptable warehouse spaces can provide the flexibility needed to tailor a property to precise operational needs, offering a significant advantage in rapidly evolving markets.

Understanding Space Configurations

Commercial warehouses are far from monolithic; they come in a variety of configurations designed to meet diverse business needs. Understanding these distinctions is key to selecting the most appropriate space.

Industrial Space: This category typically refers to properties primarily used for manufacturing, production, storage, or distribution. Large open areas, high ceilings, heavy power, and robust loading capabilities characterize these spaces. They are often found in industrial parks, strategically located near major transportation arteries.

Office Components: Many industrial warehouses integrate office components, ranging from a small administrative area to substantial corporate offices. These spaces are crucial for businesses that require on-site management, sales teams, or customer service operations alongside their warehouse activities. The ratio of office to warehouse space can vary significantly, impacting functionality and rental rates.

Flex Units: Flex spaces are a hybrid, offering a balanced mix of industrial (warehouse/light manufacturing) and office space. They are highly versatile, catering to businesses that need both production/storage and administrative functions within a single unit. Think of them as adaptable shells that can be customized for a wide array of uses, from R&D labs to showrooms with back-end storage.

Multi-Tenant Facilities:These properties house multiple businesses under one roof, with individual units leased out. They often provide shared amenities such as common loading docks, parking, and, in some cases, shared office services. Multi-tenant facilities are particularly attractive to smaller businesses that may not require an entire standalone warehouse but still need dedicated industrial or flex space.

Build-to-Suit Options: For businesses with highly specific or unique requirements, a build-to-suit option allows a developer to construct a custom facility tailored precisely to the tenant’s specifications. While this typically involves longer lease terms and higher costs, it ensures optimal functionality and efficiency for specialized operations.

Each configuration offers distinct advantages, and the optimal choice depends heavily on a business’s operational model, growth projections, and specific functional needs.

Strategic Location and Accessibility

The adage “location, location, location” holds profound truth in commercial real estate, particularly for warehouses. Strategic location and accessibility are critical determinants of operational efficiency, cost-effectiveness, and market reach.

Transit Scores: While often associated with residential properties, transit scores can indirectly impact commercial warehouse accessibility for employees and, in some cases, for smaller delivery vehicles using public transport routes. More directly, proximity to public transportation can be a significant factor for businesses with large workforces.

Highway Proximity:Direct and easy access to major highways and interstates is non-negotiable for most warehouse operations. This minimizes truck transit times, reduces fuel costs, and facilitates faster distribution of goods, directly impacting a business’s bottom line.

Logistics Hubs:Locating a warehouse within or near established logistics hubs – areas with a high concentration of transportation infrastructure, such as intermodal yards, airports, and major freight routes – offers unparalleled advantages. These hubs streamline supply chain operations, providing access to a network of carriers and distribution services.

Last-Mile Delivery: With the explosion of e-commerce, the efficiency of last-mile delivery has become a competitive differentiator. Warehouses positioned closer to urban centers or densely populated areas can significantly reduce last-mile delivery times and costs, which is crucial for meeting customer expectations.

Shipping Efficiency: Overall shipping efficiency is a composite of all these factors. A well-located warehouse minimizes bottlenecks, optimizes delivery routes, and reduces the time goods spend in transit. This not only enhances customer satisfaction but also contributes to a more sustainable and cost-effective supply chain.

Considering these strategic location factors is vital for any business looking to lease a commercial warehouse, as they directly influence operational performance and market competitiveness in May 2026.

Optimizing Operations for HVAC and Plumbing Contractors

For HVAC and plumbing contractors, the right commercial warehouse for lease can be a game-changer, transforming daily operations and supporting business growth. These specialized trades require spaces beyond simple storage, demanding facilities that optimize inventory management, securely house valuable equipment, and provide efficient staging areas.

A well-designed warehouse enables systematic inventory management, ensuring that parts, pipes, and units are easily accessible and reducing wasted time searching for materials. Secure equipment storage is paramount, protecting expensive tools, machinery, and vehicles from theft and damage. Dedicated fleet parking, ideally secured and with easy ingress/egress, streamlines the dispatch process and enhances vehicle security. A centralized dispatch office within the facility can improve communication and coordination for service calls. The goal is centralized logistics, where all operational components – from receiving supplies to preparing for jobs – are integrated under one roof. Workshop requirements, such as specialized bays for repairs, fabrication, or pre-assembly, can significantly boost productivity. The right space acts as a catalyst for business expansion, enabling contractors to take on more projects and serve a larger client base.

Streamlining Service Workflows

The efficiency of an HVAC or plumbing contractor’s service workflow is directly tied to the functionality of their operational base. A well-chosen commercial warehouse can dramatically streamline these processes.

Tool Organization:Implementing a robust system for tool organization within the warehouse ensures that technicians can quickly grab what they need before heading to a job site. This might involve dedicated racks, shadow boards, or mobile tool carts.

Material Staging:Designated areas for material staging enable efficient preparation of job-specific kits. Materials for upcoming projects can be gathered and organized in advance, minimizing delays and ensuring technicians arrive on-site fully equipped.

Rapid Response: A strategically located, well-organized warehouse enables rapid response to emergency calls. Technicians can quickly access necessary parts and equipment, reducing client downtime and enhancing customer satisfaction.

Loading Bay Access: Easy, unobstructed access to loading bays is crucial for both receiving large deliveries of equipment and loading service vehicles with heavy or bulky items. Drive-in bays are particularly beneficial for smaller vehicles, while dock-high bays serve larger delivery trucks.

Administrative Integration: Integrating administrative functions within the same facility enables seamless communication among field teams, dispatch, and office staff. This can include dedicated desks for paperwork, invoicing, and customer support, ensuring that the back-end operations support the front-line service delivery.

By optimizing these elements, contractors can reduce operational friction, improve productivity, and ultimately deliver higher quality service.

Professionalism and Client Perception

For HVAC and plumbing contractors, their physical premises can significantly impact their professionalism and client perception. A well-maintained and functional commercial warehouse can project an image of reliability and competence.

Showroom Potential: Some flex spaces within a commercial warehouse can be designed with showroom potential, allowing contractors to display high-end HVAC units, plumbing fixtures, or innovative solutions to clients. This provides a professional environment for consultations and product demonstrations.

Meeting Spaces: Dedicated meeting spaces, distinct from the workshop or storage areas, offer a professional setting for client consultations, team meetings, and vendor presentations. This elevates the contractor’s image beyond that of a mere service provider.

Brand Visibility: A clean, organized exterior with prominent signage enhances brand visibility and reinforces a professional image. A dilapidated or disorganized facility, conversely, can undermine client confidence.

Secure Storage: Demonstrating robust secure storage for client equipment or high-value parts reassures clients that their assets are protected. This is particularly important for longer-term projects or specialized components.

Operational Efficiency: Clients often infer a company’s professionalism from its operational efficiency. A well-organized warehouse that enables quick service turnaround and accurate inventory management signals a competent and reliable business.

Investing in a commercial warehouse that supports professionalism and client perception is a strategic move that can differentiate a contractor in a competitive market.

MicroFlex™: Redefining Small Business Infrastructure in Alabama

MicroFlex™ is at the forefront of redefining small-business infrastructure, particularly in Alabama’s burgeoning markets. We recognize that traditional commercial leases often present significant hurdles for small- to medium-sized enterprises (SMEs), including rigid terms and unsuitable space configurations. Our approach is centered on providing comprehensive small-business support through highly flexible, multi-functional spaces.

We believe that the right environment can be a catalyst for growth. Our facilities are designed to foster growth-oriented environments, offering adaptable units that can evolve as a business’s needs change. This commitment extends to cultivating a vibrant entrepreneurial community within our spaces, where businesses can network, collaborate, and thrive. By offering tailored solutions, MicroFlex™ empowers businesses to focus on their core operations without being constrained by inadequate or inflexible real estate.

Strategic Alabama Locations

Our strategic presence across Alabama is designed to serve key economic hubs and provide unparalleled regional connectivity. We have carefully selected locations that offer optimal logistical advantages and access to growing markets.

Birmingham-Irondale:Located within the greater Birmingham metropolitan area, our Irondale location benefits from proximity to major interstates and a diverse industrial base, making it ideal for distribution, light manufacturing, and service-oriented businesses.

Auburn: Serving the dynamic Auburn-Opelika region, this location caters to businesses tapping into the university ecosystem, tech startups, and the growing retail and service sectors.

Birmingham-Hoover: Another prime location within the Birmingham metro, Hoover offers access to a robust consumer market and a skilled workforce, suitable for a wide range of commercial operations.

Huntsville-Madison: As a hub for aerospace, technology, and advanced manufacturing, our Huntsville-Madison facilities are perfectly situated for businesses requiring specialized industrial and flex spaces, benefiting from the region’s innovative economy.

These strategically chosen locations ensure that MicroFlex™ clients benefit from excellent accessibility, strong local economies, and the infrastructure necessary for sustained growth, reinforcing Alabama’s position as a burgeoning commercial landscape.

Why MicroFlex™ is the Premier Alternative

MicroFlex™ stands out as the premier alternative to conventional commercial warehouse leasing, particularly for businesses seeking agility and tailored solutions. We are dedicated to eliminating roadblocks that often hinder small and growing enterprises. Our business model is built on providing simplified logistics, enabling our clients to move in, operate, and scale with minimal friction.

We offer scalable footprints, meaning businesses can easily expand or contract their space as their needs change, without the burden of long-term, inflexible commitments. This adaptability is a cornerstone of our service, enabling businesses to pivot more effectively and grow faster. Our approach is business-centric management, where we act as a partner, providing responsive support and a conducive environment for success. By removing long-term constraints typically associated with traditional leases, MicroFlex™ empowers entrepreneurs to innovate and thrive.

Feature

Traditional Industrial Leases

MicroFlex™ Flexible Solutions

Lease Term

Typically 3–10+ years, often rigid

Flexible, shorter terms, including month-to-month options

Space Scalability

Difficult to expand or contract without a new lease or sublease

Easy to scale up or down within the same facility

Upfront Costs

High (security deposits, tenant improvements, legal fees)

Lower and more manageable

Customization & Flexibility

Limited; often requires significant tenant investment

Designed for multi-functional use with adaptable layouts

Maintenance & Utilities

Often the tenant’s responsibility (NNN lease)

Frequently included or simplified, reducing operational burden

Operational Control

High level of control, but with greater responsibility

Shared or managed services allow businesses to focus on core operations

Community

Typically isolated from other businesses

Encourages an entrepreneurial environment with networking opportunities

Best Suited For

Large, established businesses with stable space requirements

Small businesses, startups, e-commerce companies, contractors, and seasonal operations

Frequently Asked Questions

1. What are the primary types of commercial lease structures?

In May 2026, the commercial real estate market primarily utilizes three main lease structures, each with distinct implications for tenants and landlords.

NNN (Triple Net) Leases: Under an NNN lease, the tenant is responsible for paying a base rent plus a prorated share of the property’s operating expenses, including property taxes, building insurance, and common-area maintenance (CAM) fees. This structure is common in industrial and retail properties, offering landlords a more predictable income stream.

Gross Leases: In a gross lease, the tenant pays a single, all-inclusive rental payment, and the landlord covers all property operating expenses. While simpler for the tenant, it’s important to clarify what “all-inclusive” truly means, as utilities are often excluded.

Full-Service Leases: Often found in multi-tenant office buildings, a full-service lease is similar to a gross lease but typically includes all operating expenses and utilities, as well as janitorial services. This offers the most predictability for tenants regarding monthly costs.

Common Area Maintenance (CAM) Fees: These are charges tenants pay landlords to cover the maintenance, repair, and operation of common areas within a commercial property, such as parking lots, landscaping, hallways, and security. CAM fees are typically found in NNN and sometimes modified gross leases.

2. How do businesses determine the necessary warehouse size?

Determining the optimal warehouse size is a critical decision that impacts efficiency and cost. In May 2026, businesses typically consider several key factors:

Inventory Volume: The current and projected volumes of goods to be stored are the primary determinants. This includes raw materials, work-in-progress, and finished products.

Equipment Dimensions: The size and maneuverability requirements of material handling equipment (e.g., forklifts, pallet jacks) dictate aisle widths and turning radii.

Staffing Levels: The number of employees working in the warehouse influences the need for office space, break rooms, restrooms, and adequate circulation areas.

Future Growth Projections: It’s crucial to anticipate future business expansion. Leasing a space that offers room for growth or the flexibility to expand within the same complex can prevent costly relocations down the line.

Ceiling Height Requirements: High clear heights allow for vertical storage, significantly increasing usable space without expanding the physical footprint. This can be a more cost-effective way to accommodate growing inventory.

3. What factors influence commercial property demand in May 2026?

Several interconnected factors are shaping commercial property demand in May 2026:

Supply Chain Shifts: Ongoing global supply chain disruptions and the drive for resilience are leading companies to re-evaluate their logistics networks, often increasing demand for strategically located warehousing and distribution centers closer to end-consumers or key transportation hubs.

Technological Integration: The adoption of automation, AI, and IoT in logistics and manufacturing is influencing warehouse design, favoring properties that can accommodate advanced robotics, smart inventory systems, and higher power requirements.

Urbanization: Continued population growth in urban and suburban areas drives demand for last-mile delivery facilities and mixed-use developments that integrate commercial spaces into community living.

Sustainability Standards: There’s a growing emphasis on green buildings and sustainable operations. Properties with energy-efficient designs, renewable energy sources, and eco-friendly features are increasingly attractive to tenants and investors, influencing demand.

Flexible Workspace Trends: The hybrid work model continues to evolve, impacting office space demand. However, it also creates opportunities for flex office solutions and integrated warehouse-office (flex) spaces for businesses that need both collaborative and operational areas.

Conclusion

Navigating the dynamic landscape of commercial warehouse leasing in May 2026 requires strategic planning and a keen understanding of market nuances. For businesses, securing the right space is not merely a logistical decision but a strategic imperative that underpins operational agility and market resilience. By carefully evaluating essential criteria such as space configuration, location, and lease structures, companies can future-proof their operations and position themselves for sustained growth.

Whether you are an HVAC contractor optimizing service workflows or a small business seeking scalable infrastructure, the right commercial property can unlock significant potential. In regions like Alabama, innovative solutions are emerging to meet these evolving demands. Partnering with a professional team that understands your unique needs can transform the complex process of finding a commercial warehouse for lease into a streamlined and successful endeavor, fostering business growth and operational excellence.

https://www.strategydriven.com/wp-content/uploads/IMG_2069.jpeg10801620StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2026-06-02 21:36:272026-06-02 21:36:27Navigating Commercial Real Estate: Flexible Spaces and Financing Solutions