Knoxville, Tennessee, is undergoing a remarkable period of growth and transformation. Nestled at the foothills of the Great Smoky Mountains, this city has become a dynamic destination for new residents and investors seeking a blend of affordability, culture, and opportunity. The evolving real estate landscape is at the heart of Knoxville’s continued development, reshaping both its skyline and community spirit. With an ever-increasing number of newcomers, building connections and navigating the local housing market are more important than ever.

Guiding buyers, sellers, and investors through these exciting changes are experienced professionals like Knoxville TN real estate agent Bessie Whiteside. Bessie Whiteside, a standout expert in Knoxville’s real estate scene, is known for her deep knowledge of the area and commitment to helping clients find the right property solutions in East Tennessee. As the owner of a leading realty website, Whiteside serves both newcomers and longtime residents with personalized guidance that makes the transition seamless and rewarding. Her service area covers Knoxville and the surrounding regions, making her brand a trusted resource for anyone considering a move to this vibrant city.

Knoxville’s Real Estate Boom

Over the past several years, Knoxville has emerged as one of Tennessee’s most compelling real estate hotspots. The city’s competitive cost of living, attractive employment opportunities, and growing reputation as a lifestyle destination are fueling demand for homes from a variety of buyers. Young professionals, families, and retirees alike are being drawn to Knoxville’s neighborhoods, driven by the promise of economic growth and a high quality of life. As a result, the property market is thriving, offering both stability for investors and opportunity for new residents.

In addition to affordability, Knoxville’s diversity is boosting its real estate market. Both in-town and suburban areas offer a spectrum of living options, from heritage homes near downtown to modern, amenity-rich developments. The influx of residents is not only revitalizing established communities but also supporting the launch of new developments, all contributing to a vibrant, interconnected city fabric.

Urban Development and Infrastructure

Parallel to the surge in housing demand, Knoxville’s cityscape is being transformed by ongoing urban development projects. Signature undertakings, such as the new plaza at the Gay Street Bridge and a wave of apartment complexes, are reshaping downtown. These additions enhance Knoxville’s livability, offering improved public spaces, new retail, and expanded housing for a growing population. As the skyline evolves, these projects also inject economic energy, fueling job creation and attracting fresh businesses to the area.

Beyond the visible changes, infrastructure improvements are making a real difference for residents. Upgraded roads, renovated public amenities, and increased investment in transportation have all enhanced accessibility and convenience across Knoxville. These city-led initiatives ensure that growth benefits current residents while laying the foundation for continued prosperity.

Community Impact

The growth in Knoxville’s real estate sector is shaping neighborhoods in profound ways. As new residents arrive and housing options expand, local businesses have seen a surge in patronage, fostering a diverse economic landscape. New retail spaces and restaurants pop up alongside established mainstays, infusing Knoxville’s community with fresh energy.

Increased diversity is reflected in an expanding cultural scene. Events, festivals, and community gatherings draw on the city’s rich traditions and the talents of new arrivals. This melding of old and new creates a sense of belonging and connectivity, with residents of all backgrounds finding common ground in Knoxville’s welcoming environment. Resourceful organizations and neighborhood associations further strengthen community ties, promoting collaboration and support for both new and established locals.

The Role of Real Estate Professionals

Navigating a fast-growing real estate market requires expertise and local knowledge. Trusted real estate agents like Bessie Whiteside are essential guides, helping newcomers interpret market trends, explore neighborhoods, and secure homes that match their needs. Their services include everything from staging and marketing properties to negotiating transactions, ensuring a smooth experience for clients at every step. By working closely with buyers and sellers, professionals like Whiteside help stabilize the market and foster sustainable growth in Knoxville’s housing sector.

Challenges and Considerations

Despite Knoxville’s positive momentum, growth brings certain challenges. Rising demand can drive up home prices, raising questions about long-term affordability for some residents. Infrastructure, while improving, sometimes faces strain due to the rapid influx of new arrivals and development. Local officials and city planners are actively addressing these concerns, seeking policies and projects that ensure accessibility, preserve neighborhood character, and protect Knoxville’s charm amid ongoing change.

Looking Ahead

Knoxville’s real estate momentum shows no signs of slowing. As the city continues to invest in infrastructure and support community-driven growth, it remains a top destination for those seeking a fresh start or lucrative investment. New projects on the horizon, coupled with a robust spirit of innovation, promise even more opportunities for residents and businesses alike.

Conclusion

More than just a market trend, Knoxville’s real estate boom is a transformative force shaping the city’s future. New developments, a strong sense of community, and dedicated local professionals are working together to create a place where people of all backgrounds can prosper. For anyone considering a move or investment in East Tennessee, Knoxville stands ready to welcome and inspire the next generation of homeowners, entrepreneurs, and neighbors.

https://www.strategydriven.com/wp-content/uploads/IMG_1676.jpeg9001364StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2026-05-04 21:36:182026-05-04 21:36:18Knoxville’s Thriving Real Estate Market: Transforming Community and Opportunity

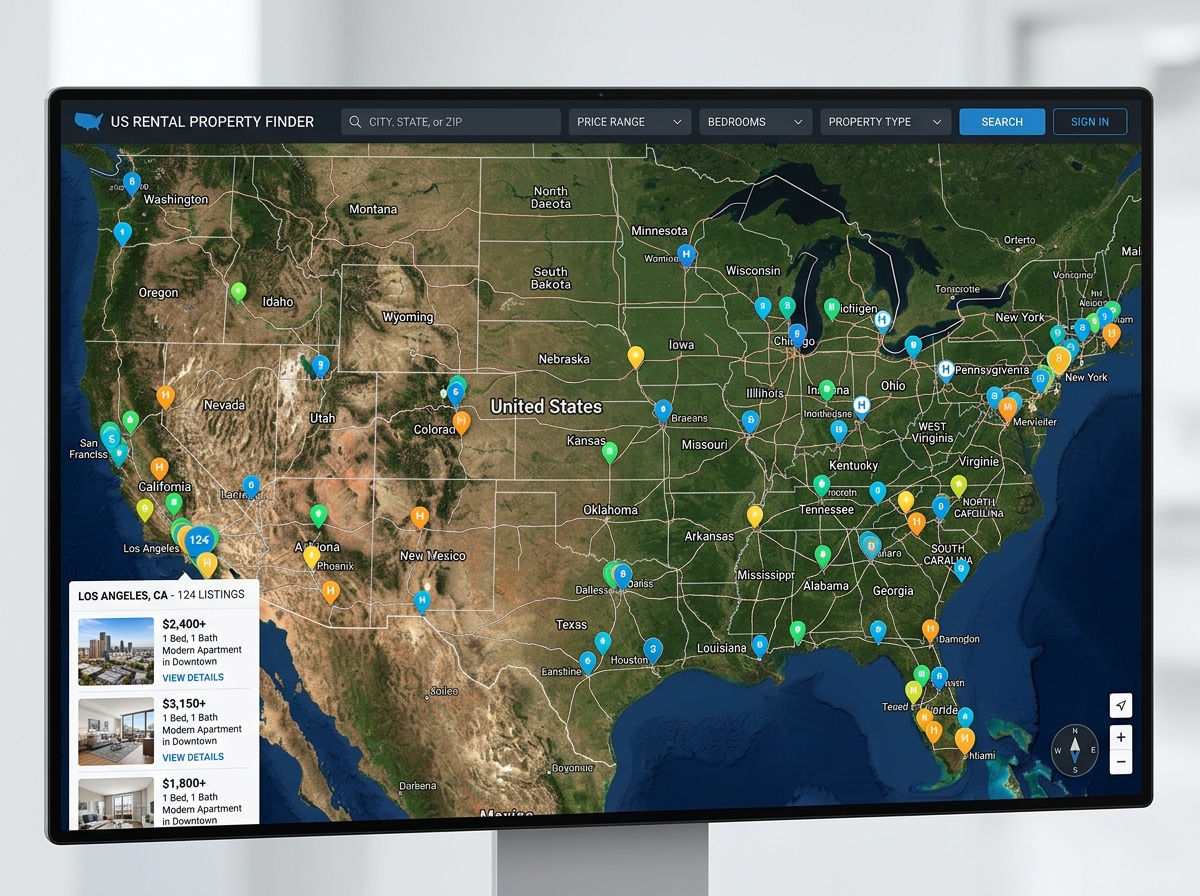

Navigating the Landscape of Real Estate and Property Rentals

The landscape of real estate and property rentals is constantly evolving, presenting both opportunities and challenges for individuals and investors alike. As we move through April 2026, understanding the current market dynamics is more crucial than ever. Whether you are searching for your next home, managing a property, or simply exploring investment possibilities, up-to-date information is your most valuable asset.

We will delve into the latest rental market trends across the United States. We will compare inventory levels and average rent prices in different states, highlighting both the most affordable and the highest-priced regions. We will also examine how leading platforms present their listings and the resources they provide. Our goal is to offer clear insights and practical solutions to help you navigate the modern world of property rentals. For comprehensive Real estate insights and tools, exploring dedicated resources can be highly beneficial.

The rental market in April 2026 is characterized by dynamic shifts in inventory levels and average rent prices, reflecting a complex interplay of economic factors, population movements, and regional development. Understanding these market trends is paramount for anyone involved in property rentals, from prospective tenants to seasoned investors. We observe distinct patterns emerging across various US states, painting a diverse picture of availability and affordability.

National Inventory and Pricing Trends

As of April 2026, the rental market shows significant variation in availability. Florida leads with 65,293 properties for rent, commanding an average rent price of $4,245. This high inventory, coupled with a robust average price, indicates strong demand and a competitive market. Texas follows with a substantial 41,205 properties available, but with a more accessible average rent of $2,298, suggesting a broader range of options for various budgets.

California, despite its reputation for high costs, shows a surprisingly low inventory of 878 properties for rent, yet an exceptionally high average rent price of $11,447. This disparity points to extreme scarcity in available listings, driving up prices significantly for the limited options. New York state, another high-cost region, lists 6,691 properties with an average rent of $8,725. Other states also present notable figures: Arizona with 8,281 properties averaging $3,306, New Jersey with 11,700 properties at $4,585, Massachusetts with 8,110 properties at $3,929, and Pennsylvania with 8,545 properties averaging $2,371.

These figures illustrate that while some states offer a large volume of rentals, others, particularly those with high demand and limited space, struggle with inventory, leading to inflated prices.

To provide a clearer snapshot, here’s a comparison of selected states:

State

Number of Properties for Rent (April 2026)

Average Rent Price (April 2026)

Florida

65,293

$4,245

Texas

41,205

$2,298

California

878

$11,447

New York

6,691

$8,725

Pennsylvania

8,545

$2,371

Regional Market Drivers

The dynamics of supply and demand are central to these market variations. States experiencing significant economic growth, such as Florida and Texas, often see an influx of new residents, increasing demand for housing. This growth can be fueled by job creation, business relocation, and attractive lifestyle factors. Consequently, the rental market expands to accommodate these new populations, as evidenced by their high property counts.

Population shifts also play a crucial role. Areas that are growing rapidly due to migration, whether for work or retirement, naturally experience heightened competition for rentals. Conversely, inventory shortages in rural areas, like those sometimes found in states such as Arkansas, can be due to lower population density and less development, or simply a tight local market where properties are quickly leased. For those exploring opportunities in such regions, resources like Arkansas Homes and Rentals can offer localized insights.

Factors influencing these trends include local economic health, job markets, and the availability of new construction. In areas with robust economies and limited new housing development, prices tend to climb. Understanding these regional drivers is key to anticipating market shifts and making informed decisions in the rental sector.

Regional Variations in Rental Market Pricing

The cost of renting property across the United States in April 2026 is far from uniform. Significant disparities exist, driven by a confluence of factors including economic prosperity, population density, and the fundamental balance between housing supply and demand. These variations create distinct rental landscapes, from the ultra-expensive urban centers to more budget-friendly regions.

High-Demand Urban Centers and Real Estate and Property Rentals

High-demand urban centers, particularly those with thriving economies and limited space for expansion, consistently exhibit some of the highest rental prices. New York, NY, stands out as a prime example, with a staggering 15,637 to 17,157 rental listings available, yet commanding an average rent price of $8,725 across the state. In New York City itself, studios can start from $2,950+, one-bedrooms from $3,224+, and two-bedrooms can reach upwards of $6,800+. This reflects intense competition and a premium on urban living.

California pricing, particularly in its major metropolitan areas, is another benchmark for high costs. With an average rent of $11,447 for a mere 878 properties statewide, the market is characterized by extreme scarcity and exorbitant prices. This situation is particularly acute in cities like Los Angeles, where the demand for housing far outstrips supply. For those navigating the complexities of this market, understanding the local nuances is critical. Insights into the Los Angeles real estate market reveal the unique pressures and opportunities present in such a competitive environment. Factors influencing these high prices include robust job markets in tech and entertainment, desirable climates, and stringent zoning regulations that limit new construction. The inventory scarcity in these regions means that even modest properties come with a significant price tag, making affordability a major challenge for many residents. For those considering a move to Florida, especially in later life, exploring options in Adult Communities in Florida might offer different pricing structures and amenities.

Affordable Housing Opportunities

While the spotlight often falls on high-cost areas, the US rental market also offers numerous affordable housing opportunities. Pennsylvania, for instance, presents a more accessible market with an average rent of $2,371 for its 8,545 properties. This makes it an attractive option for renters seeking more value for their money without necessarily sacrificing quality of life. The state’s diverse economy and lower cost of living contribute to its relative affordability compared to coastal hubs.

Similarly, Texas affordability continues to draw residents, with an average rent price of $2,298 across its 41,205 properties. This combination of ample inventory and competitive pricing positions Texas as a strong contender for those prioritizing budget-friendly options. The state’s expansive land, business-friendly environment, and ongoing development contribute to a more balanced housing market. For individuals or families looking for newer housing options in such growing markets, investigating New Construction Homes in Texas can be a valuable approach. Furthermore, regions like Montgomery County, TN, also offer compelling rental options, as highlighted by resources such as Montgomery County, TN Apartments & Homes for Rent | Compass. These areas often provide a good balance of community amenities, employment opportunities, and reasonable rental costs, making them ideal for a wide range of renters.

The contrast between these high-cost and affordable regions underscores the importance of researching specific markets when planning a rental search. What might be considered a standard rent in one state could be a luxury in another, and vice-versa.

Essential Amenities and Property Features

Beyond location and price, the amenities and specific features of a rental property significantly influence its appeal and value. In today’s competitive rental market, properties equipped with desirable amenities can stand out, attracting tenants and commanding higher rents. From the practical to the luxurious, understanding what features are commonly highlighted and which are considered rare can guide both renters in their search and landlords in their investments.

For those seeking temporary living solutions, especially in bustling urban centers, the availability of furnished properties can be a game-changer. For example, in a city known for its automotive heritage and revitalized urban core, Detroit furnished real estate rentals cater to professionals, students, and short-term residents who require move-in ready accommodations. Similarly, for vacationers, specific amenities are paramount. Coastal destinations often feature unique offerings; for instance, Vacation Rentals in Gulf Shores | Beach Houses & Condos emphasize proximity to beaches, private pools, and spacious layouts suitable for family getaways.

Common and Rare Amenities

Certain amenities have become almost standard expectations in modern rental properties. Pet-friendly features, for example, are increasingly sought after, reflecting the growing number of households with pets. Smart home technology, offering convenience and energy efficiency, is also gaining traction. However, the prevalence of these amenities can vary significantly by location and property type.

In high-density markets like New York, NY, where space is a premium, some amenities that might be common elsewhere are considered rare luxuries. According to recent data, swimming pools are available in only about 18% of New York rentals, making them a highly desirable and often premium feature. Clubhouses, which offer communal space and recreational opportunities, are found in just 12% of listings. Even more niche, pet washing stations, a boon for pet owners, are present in only 7% of properties. Patios, offering private outdoor space, are also notably rare, appearing in just 9% of New York rentals. This scarcity drives up the value of properties that do offer them.

Beyond the urban core, other property types offer different amenity sets. For those interested in a specific housing style, finding Townhouses in Frederick, MD might reveal common features like private garages or small yards, which are less common in apartment complexes.

Property Type Comparisons

The type of property also dictates the available features. Single-family homes, for instance, typically offer more privacy, yard space, and often come with garages or driveways. For families or individuals desiring more space and a suburban feel, exploring options like Houses for Rent in Burke, VA can highlight such benefits.

Luxury condos, on the other hand, often boast high-end interior finishes, concierge services, fitness centers, and rooftop access, appealing to those seeking convenience and upscale living. In recreational areas, specific property types cater to leisure. For example, Condos in Osage Beach, MO might feature lake access, boat slips, and resort-style amenities. Studio apartments are designed for efficiency and affordability, typically offering compact living spaces ideal for single occupants or those on a tighter budget. Multi-family units, ranging from duplexes to large apartment complexes, can offer a spectrum of amenities depending on their scale and target demographic.

Understanding these amenity and property type distinctions is crucial for both renters refining their search criteria and property owners looking to maximize their property’s marketability.

Digital Tools for Modern Renters and Landlords

The digital revolution has profoundly transformed the real estate and property rentals landscape, empowering both renters and landlords with an array of sophisticated tools. In April 2026, technology plays an indispensable role in streamlining every aspect of the rental process, from initial search and application to lease management and rent collection. These digital solutions enhance efficiency, transparency, and accessibility, making the market more navigable for everyone.

Major real estate platforms now offer a suite of features designed to assist users. For renters, this includes advanced search filters that allow them to pinpoint properties based on specific criteria like location, price range, number of bedrooms, and desired amenities such as swimming pools or pet-friendly policies. Many platforms also provide affordability calculators, which help prospective tenants understand how much rent they can realistically afford based on their income and other financial commitments. Real-time alerts notify renters the moment new listings that match their preferences hit the market, ensuring they don’t miss out on opportunities in fast-moving areas.

For landlords and property managers, digital tools are equally transformative. These include comprehensive tenant screening services that facilitate background checks, credit reports, and rental history verification. Online rent collection systems simplify financial transactions, offering convenience and secure payment options. Lease creation and digital signing functionalities expedite the paperwork, while property management dashboards provide an overview of vacancies, maintenance requests, and financial performance.

For individuals contemplating their housing future, digital tools are invaluable for strategic planning. Rent vs. buy analysis calculators help prospective homeowners weigh the financial implications of renting against purchasing a property, considering factors like mortgage interest, property taxes, and potential appreciation. Mortgage calculators provide estimates of monthly payments, allowing users to assess their borrowing capacity. For a comprehensive overview of financial readiness, utilizing a House Affordability Tool can be a crucial first step.

Furthermore, these platforms often integrate agent finders, connecting users with local real estate professionals who can offer expert guidance. Access to detailed market reports provides insights into local trends, property values, and investment opportunities, enabling more informed decision-making. These resources collectively empower users to make strategic choices whether they are looking to rent, buy, or invest in real estate.

Professional Resources for Property Management

Property management has been significantly streamlined by digital innovation. Landlord tools offered by leading services provide a centralized hub for managing all aspects of rental properties. This includes advertising vacancies to a wide audience, managing digital applications, and facilitating online lease agreements. The ability to collect rent online not only enhances convenience but also improves payment tracking and reduces administrative burdens.

Beyond transactional tools, these platforms also serve as vital resources for understanding legal frameworks. They often provide information on tenant rights and fair housing protections, helping landlords ensure compliance and fostering positive tenant relationships. For more specific financial planning, tools like a Mortgage Calculator can help landlords assess potential investment returns, while a Refinance Calculator can assist in optimizing financing strategies for existing properties. The integration of these professional resources ensures that property management is efficient, compliant, and financially sound.

Frequently Asked Questions about Real Estate and Property Rentals

Navigating the real estate and property rentals market can often lead to a myriad of questions. Here, we address some of the most common inquiries to provide clarity and guidance for both renters and those interested in market dynamics.

1. Which states currently offer the most affordable rental properties?

As of April 2026, based on available data, Texas and Pennsylvania stand out as states offering some of the most affordable rental options. Texas boasts an average rent price of $2,298 across its 41,205 properties, making it an attractive destination for many. Pennsylvania follows closely with an average rent of $2,371 for its 8,545 properties. These states generally offer a lower cost of living compared to coastal regions and major metropolitan areas, coupled with diverse economies that support a range of housing prices. The higher inventory levels in Texas also contribute to more competitive pricing, giving renters more options. Factors like land availability for new development and a less saturated market contribute to their relative affordability.

2. What amenities are considered rare in high-density markets like New York?

In high-density markets such as New York, NY, certain amenities that might be common elsewhere are considered rare and add significant value to a rental property. Based on recent market insights, swimming pools are notably rare, found in only about 18% of rental listings. Clubhouses, which provide communal and recreational spaces, are present in just 12% of properties. For pet owners, pet washing stations are an uncommon luxury, available in only 7% of rentals. Additionally, private outdoor patios are also quite scarce, appearing in approximately 9% of listings. The limited space and high cost of construction in dense urban environments contribute to the rarity and premium pricing of these amenities.

3. How can renters determine their ideal budget for a new property?

Determining an ideal budget for a new rental property involves a combination of personal financial assessment and market understanding. Renters should utilize affordability calculators provided by major real estate platforms, which typically suggest that rent should not exceed 30% of one’s gross monthly income. This is a common guideline, though it can vary based on individual financial situations and local cost of living.

It’s also crucial to consider income-to-rent ratios and factor in all potential expenses beyond just the monthly rent, including utility costs (electricity, gas, water, internet), renter’s insurance, parking fees, and pet fees if applicable. Understanding local market trends can also help set realistic expectations for prices in desired neighborhoods. By comprehensively assessing income, expenses, and market realities, renters can establish a sustainable budget that prevents financial strain and ensures a comfortable living situation.

Conclusion

The real estate and property rentals market in April 2026 is a dynamic and multifaceted environment, offering a spectrum of opportunities and challenges. From the high-demand, high-cost urban centers of California and New York to the more affordable and expansive markets of Texas and Pennsylvania, understanding regional variations is key. The availability of properties, average rent prices, and the prevalence of essential amenities all play critical roles in shaping the rental experience for individuals and the investment landscape for property owners.

Modern digital tools have revolutionized how we search, manage, and interact with rental properties, providing renters with powerful search capabilities and affordability calculators, and equipping landlords with efficient tenant screening and online management systems. As we continue to navigate this evolving market, leveraging these resources and staying informed about current trends will be paramount. Whether you are seeking your next home or managing an investment, market expertise and local partnerships are invaluable in finding the perfect fit. We encourage you to Explore more real estate listings and utilize the wealth of information available to make confident, informed decisions in your real estate journey.

https://www.strategydriven.com/wp-content/uploads/IMG_1652.jpeg10111363StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2026-04-23 21:43:502026-04-23 21:43:50Modern Solutions for Real Estate and Property Rentals

Have you ever looked at a perfectly trimmed lawn and thought, “Someone is making serious money off this”? Landscaping may seem simple, but building a profitable company takes more than a mower and good weather. It sits at the crossroads of rising home values, climate concerns, and a growing desire for outdoor living spaces. This article breaks down the key steps, from planning to scaling, with practical insights and a few honest observations about what actually works.

Understanding the Market You’re Entering

Landscaping demand has quietly surged alongside the work-from-home shift. People now care more about their yards because they spend more time in them, and real estate trends show outdoor upgrades can boost property value. That means opportunity, but also competition from established crews and DIY-minded homeowners.

Start by studying your local market closely. Look at pricing, services offered, and customer expectations. A suburban neighborhood may want weekly lawn care, while higher-end clients may demand full landscape design and irrigation systems. The clearer your niche, the easier it becomes to stand out and avoid being just another guy with a truck.

Building a Strong Foundation from Day One

Launching a landscaping company without structure often leads to burnout or thin margins. Early decisions about licensing, insurance, and service packages shape long-term success more than most beginners realize. You want systems, not chaos disguised as hustle.

Many new owners find it helpful to begin with a professional landscaping business startup kit. This approach prevents costly mistakes like underpricing jobs or buying tools you rarely use. Solid planning also signals professionalism to clients who are increasingly cautious about who they hire.

Pricing Services for Profit, Not Just Survival

A common mistake is pricing based on what competitors charge without understanding costs. Fuel, labor, maintenance, and time all add up quickly, and ignoring even one factor can erase profit. In a time when inflation affects everything from gas to fertilizer, guessing is not an option.

Break down each service into hourly costs and add a margin that supports growth. For example, mowing is not just about time spent cutting grass; it includes travel, equipment wear, and cleanup. Clear pricing also builds trust, especially when customers are comparing quotes online and expecting transparency.

Investing in the Right Equipment

Buying equipment feels like progress, but it can easily become a financial trap. High-end tools look impressive, yet many new businesses overspend before securing steady clients. The goal is efficiency, not showing off your gear.

Start with reliable basics like a commercial mower, trimmer, and blower. As revenue grows, reinvest in tools that save time or expand services, such as aerators or irrigation systems. With supply chain disruptions still affecting equipment availability in some regions, planning purchases ahead can prevent delays during peak seasons.

Building a Reliable Team

Landscaping is labor-intensive, and your business will eventually depend on more than your own effort. Hiring too quickly can strain finances, but waiting too long limits growth. Finding the balance is one of the toughest parts of scaling.

Look for workers who show up on time and care about quality, even if they lack experience. Training is easier than fixing a poor work ethic. Offer clear expectations and fair pay because the labor market has shifted, and good workers now have more options than ever.

Marketing That Actually Brings Clients

Marketing today is less about flyers on windshields and more about online visibility. Homeowners often search for services on their phones, read reviews, and compare before making contact. Ignoring this shift is like refusing to show up where customers already are.

Create a simple website, keep your Google Business profile updated, and encourage satisfied clients to leave reviews. Social media can also help, especially with before-and-after photos that show real results. Consistency matters more than flashy campaigns, and word-of-mouth still amplifies everything.

Managing Time and Operations Efficiently

Profit in landscaping often comes down to how well you manage your day. Poor scheduling leads to wasted fuel, missed appointments, and frustrated clients. On the other hand, a well-planned route can increase daily revenue without adding more jobs.

Use scheduling software or even a detailed calendar to group jobs by location. Track how long tasks actually take so future estimates improve. Efficiency is not just about speed; it is about reducing friction in every part of your workflow, from loading equipment to billing customers.

Expanding Services for Long-Term Growth

Once the basics are running smoothly, growth comes from offering more value to existing clients. Simple add-ons like seasonal cleanups, mulching, or lighting installations can significantly increase revenue without requiring entirely new customers.

Pay attention to broader trends, such as eco-friendly landscaping or drought-resistant designs, which are gaining popularity as climate concerns rise. These services not only attract new clients but also position your business as forward-thinking. Growth is rarely about doing more of the same; it is about doing smarter work that customers are willing to pay for.

A profitable landscaping company does not happen by accident. It is built through careful planning, smart pricing, efficient operations, and a willingness to adapt to changing trends. While the work can be physically demanding, the rewards go beyond financial gain. There is something satisfying about turning a patch of grass into a space people truly enjoy, even if it sometimes means battling weeds, weather, and the occasional unrealistic client expectation.

https://www.strategydriven.com/wp-content/uploads/IMG_1647.jpeg8531280StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2026-04-23 21:02:312026-04-23 21:02:31Key Steps to Building a Profitable Landscaping Company

A Peterbilt 379 has a presence that never really goes out of style. But once you’re in the cab for hours at a time, the parts that matter most aren’t the ones people notice from the highway. They’re the upgrades that help you see clearly at night, stay comfortable on long runs, and make the truck feel like your truck instead of just another old workhorse.

That’s why the smartest interior upgrades are usually the ones that improve daily life behind the wheel. A better Peterbilt 379 cabin doesn’t need to feel flashy or overdone. It just needs to work better for the driver.

Start With Lighting That Helps You See and Relax

Interior lighting is one of the easiest ways to improve both function and style in a 379. Good lighting makes gauges easier to read, reduces the strain that comes from fighting dim or uneven cabin light, and helps the sleeper feel more usable when you’re parked for the night.

Adding Peterbilt 379 interior lights can sharpen the look of the cab while making it easier to move around in low-light conditions. That matters more than a lot of drivers expect. Better dome and accent lighting can create a cleaner, calmer space without taking away from the truck’s classic feel.

Upgrade Seating Before You Worry About Show Pieces

If you’re trying to make a 379 more enjoyable to drive, seating should be near the top of the list. Fresh upholstery, improved seat padding, better arm support, and cleaner trim can all change how the cab feels over a long day.

This kind of upgrade isn’t just about appearance. It helps reduce fatigue and gives the truck a more intentional feel. A worn seat can make the whole interior seem tired, even if the rest of the cab still has strong bones. When the seat feels right, the truck feels more capable.

Use Trim and Panels to Clean Up the Space

A lot of older Peterbilt interiors lose their appeal because the smaller surfaces start to show age first. Door panels, kick panels, headliners, and dash trim usually take a beating over time. Once they start looking rough, the cab can feel dated no matter how iconic the truck is from the outside.

Refreshing those pieces gives the interior a more complete look. The goal isn’t to make the truck feel generic. It’s to make it feel looked after. Matching materials and cleaner finishes go a long way in a 379 because they support the truck’s classic character instead of covering it up.

Don’t Ignore Visibility Improvements Inside the Cab

Night driving gets harder when the cab works against you. Glare, poor interior light placement, and cluttered surfaces can all make it more difficult to stay comfortable and focused. That’s why visibility upgrades inside the truck matter just as much as style upgrades.

Even details tied to larger power windows and upgraded interior LEDs reflect the same driver-first principle. The more easily you can read the cabin, spot what you need, and keep distractions down, the better the truck feels on the road.

Build Around the Way You Actually Drive

The best Peterbilt 379 interior upgrades aren’t random add-ons. They’re practical choices that improve comfort, visibility, and atmosphere every time you climb in. If you focus on lighting, seating, trim, and a cleaner driving environment, you’ll end up with a cab that feels more personal, more useful, and a lot more rewarding to spend time in.

https://www.strategydriven.com/wp-content/uploads/IMG_1615.jpeg10261500StrategyDrivenhttps://www.strategydriven.com/wp-content/uploads/SDELogo5-300x70-300x70.pngStrategyDriven2026-04-08 11:33:102026-04-08 11:33:10Peterbilt 379 Interior Upgrade Ideas for Comfort, Visibility, and Style

Being profitable in trading doesn’t focus solely on strategy or skill. There are various trading conditions which can affect profitability. These can be anything from commissions to spreads, leverage options and so on. A lot of the time, these will affect how profitable things get, and what return on investment you will have. That’s why it’s extremely important to know what trading conditions are, how they influence profits, and why you need to assess them carefully.

Spread Levels

One of the major trading conditions is the spread. That’s the difference between the bid price and the asking price. Spreads will usually vary a lot, based on the broker pricing, market conditions, currency pair and so on. Lower spreads make it easier to enter the market, and those can improve profits. A higher spread will reduce potential profits, but that could be an option for experienced sellers, depending on the situation.

Trading Costs and Commission Fees

As expected, there are brokers which charge commission aside from the spreads. Those commissions are charged based on the lot traded. That’s why the trader needs to calculate the total trading cost, which covers both commissions and spreads. For example, a broker that has low spreads but high commissions won’t be cheaper when compared with someone that has no commissions, yet higher spreads. It’s the reason why you always want to know the cost structure, as that will help you figure out if the strategies you are using are profitable or not.

Leverage

It’s a tool designed to help traders control larger positions while also using a small amount of capital. It can boost losses and profits. A lot of the time, Forex brokers are using leverage levels that vary depending on the account types and regulations. Leverage has great liquidity, but it also becomes a very risky trading tool.

Execution Speed

The execution speed states how quickly the trading platform will process as well as complete a trade. A quick execution is necessary due to the market prices changing way too fast. Even the slightest delay can lead to trades being executed at a bad price. And the difference between the actual price execution and the expected price is named slippage.

You will encounter slippage during high market volatility times, major economic news releases, low liquidity periods and many others. Ideally, you want to avoid any slippage. But, if that occurs often, it will lower your profitability and overall margins.

Liquidity

Clearly, liquidity refers to the ability to buy or sell assets fast, without dealing with large price changes. Forex is seen as the most liquid financial market in the world. However, there can still be variable liquidity based on the market conditions and the time of day.

Liquidity benefits traders because when it’s high, orders are executed fast, spreads remain low, and price manipulation is usually less likely to happen. However, when you have low liquidity levels, that can bring higher spreads, price gaps, difficulties exiting/entering positions and many things of that nature.

Market Volatility

It’s a great trading condition to know, because it measures how fast prices are moving in the market. If there’s high volatility, usually that means you have more trading opportunities, due to the prices changing too fast. But that also leads to higher risk. A lot of things can influence volatility, ranging from economic to interest rate changes, along with political events or worldwide economic changes.

Broker Reliability

Finding the right broker is always a challenge, because you need to perform your due diligence and focus on many different things. Those can be anything from accurate pricing to fair order execution, transparent trading conditions as well as security, especially during withdrawals. You always need to be aware of dishonest brokers that can delay withdrawals or manipulate prices, which can affect the outcome. That’s why it makes sense to only work with regulated brokers such as Exness.

Trading Platform Stability

Since the trading platform is an interface between financial markets and traders, you always want them to be very stable. But as expected, some platforms have issues like delayed order execution, disconnections, not showing the right price, frozen charts and anything of that nature. Even small issues can lead to losses, so you want to minimize those as much as possible.

Account Type Roles

You should keep in mind that brokers offer different types of accounts. Naturally, these will fit different types of traders, depending on the situation. You have the standard accounts, but also ECN accounts, professional or raw spread accounts. Every account type will offer different trading conditions, ranging from minimum deposit requirements to commissions and spreads. The best approach is to choose an account type fitting your strategy. That way, you can prevent issues, and focus on enhancing the experience in more ways than expected.

Risk Management

Even if you have great trading conditions, the reality is that you still have to be aware of risk management. The idea here is to use tools like take-profit levels, stop-loss orders, position sizing or diversification. Using such methods is a great idea if you want to limit your losses.

Evaluating the Trading Conditions

A very good idea is to compare spreads across brokers and also assess their commission structure

Test the withdrawal process and see how it works, and if there are any issues

Confirm the regulatory licenses, just to be on the safe side

Read reviews from experienced traders, so you can see if it’s ok to use that broker in the long run or not

Always test the execution speed with a demo account

Closing Thoughts

Knowing the trading conditions is extremely important because it will always affect your profitability in more ways than expected. Every factor mentioned above will play a critical role in determining the success or demise of a strategy. As always, you want to experiment with strategies, be aware of factors that can be problematic, and focus on getting the best results. It’s important to understand the pros and cons of each trading condition, how it can affect your trading approach, and then adapt accordingly to minimize losses.